✦ AI Summary

Table of Content

▲- What Is a Home Loan Balance Transfer?

- Why Transfer? The Numbers Tell the Story

- When Is the Right Time to Transfer?

- Eligibility Criteria

- Step-by-Step Process to Transfer Your Home Loan

- Costs & Charges Involved

- AquireAcres EMI Calculator for Smart Home Loan Balance Transfer Planning

- Red Flags: When a Balance Transfer Will Not Help You

- Conclusion

Home loan transfer is the most underutilised financial tool available to Indian borrowers for reducing monthly EMI and total interest outgo without changing the property or loan amount. The process shifts your outstanding loan from your current lender to a new bank or NBFC at a lower rate, and in 2026, with fully digital processing, the switch takes as little as 10–15 working days.

Most borrowers treat their home loan as a static commitment and never renegotiate the terms. A rate difference of even 0.75% on ₹50 lakh outstanding can save ₹5–7 lakhs over tenure. The guide provides information about switching times and who can switch and which expenses will be incurred and which warning signs should be watched for to help you switch safely with full financial knowledge.

What Is a Home Loan Balance Transfer?

The home loan balance transfer process allows borrowers to move their existing debt from their present lender to a different financial institution which offers reduced interest rates. The new lender pays off your old balance, and you begin fresh EMI repayments under revised, more favourable terms.

The borrower uses the same property to obtain a new loan which costs less than the original loan.

Why Transfer? The Numbers Tell the Story

Consider Rahul, a salaried professional in Pune who has an outstanding debt of ₹40 lakhs which he needs to pay back at an interest rate of 9.5% for the next 18 years, to a new lender which provides him with a lower interest rate of 8.25%.

|

Parameter |

Current Lender (9.5%) |

New Lender (8.25%) |

Difference |

|---|---|---|---|

|

Monthly EMI |

₹38,200 |

₹35,600 |

₹2,600 saved |

|

Total Interest (18 yrs) |

₹42.4 lakh |

₹36.8 lakh |

₹5.6 lakh saved |

|

Transfer Costs (est.) |

— |

₹45,000–₹55,000 |

— |

|

Break-even Period |

— |

— |

~18–21 months |

What the numbers actually mean: Rahul saves ₹2,600 every month and ₹5.6 lakhs in total interest. The break-even point occurs within 21 months after deducting transfer costs of approximately ₹50,000. The remaining 18 years of the project create a significant financial advantage. A home loan balance transfer becomes beneficial at this specific time.

Also Read: 50-30-20 Rule for Managing Your Home Loan EMI in a Tier 2 City

When Is the Right Time to Transfer?

Transfer when:

- Rate difference is at least 0.5%–0.75% or more

- You are in the early or mid-phase of tenure where interest component per EMI is highest

- Outstanding principal is above ₹20 lakhs

- Your current lender has refused to reduce your interest rate

Avoid transferring when:

- You are in the last 5–7 years of tenure, most interest is already paid

- Your lender offers a competitive retention rate reduction in writing

- You plan to fully prepay within 12 months, transfer costs will not be recovered

Eligibility Criteria

- Indian citizen or NRI, aged 23–65 years, salaried or self-employed with stable income

- The property must either be ready for immediate occupancy or currently occupied while at least 12 EMIs must have been paid without any pending payments.

- The best approval rates for a loan application require a CIBIL Score of 725 or higher.

Step-by-Step Process to Transfer Your Home Loan

- Research and compare: Use an online EMI calculator to compare rates and net savings across at least three lenders. Never apply to the first offer received.

- Negotiate internally first: Present a competing offer in writing to your current bank. Many lenders cut rates by 0.25%–0.50% to retain the account, saving you all transfer costs.

- Collect documents: Obtain the NOC and Foreclosure Letter from your current lender (~15 working days), loan account statement, and outstanding balance letter on lender's letterhead.

- Apply to new lender: Submit KYC, income proof, and property documents with the applicable processing fee.

- Sanction and closure: New lender verifies documents and issues sanction within 2–5 working days. New bank pays off the old lender; account closes and property documents are transferred.

- Set up ECS or SI: Auto-debit begins immediately. Your lower EMI starts the next payment cycle.

Costs & Charges Involved

|

Charge |

Typical Range |

|---|---|

|

Processing Fee (new lender) |

0.5%–1% of outstanding loan |

|

Legal & Technical Charges |

₹5,000–₹15,000 |

|

Stamp Duty |

As per state |

|

CERSAI Charges |

₹50–₹100 |

|

Foreclosure Fee (old lender) |

Nil for floating rate loans (RBI guideline) |

What the numbers actually mean: The complete costs of transferring funds for the ₹40 lakh loan range between ₹40,000 and ₹60,000. You will reach break-even after two years if your monthly savings from EMI payments exceed ₹2,500. The period after that point generates savings that continue until the end of the extended payment period.

Also Read: Joint Home Loan Tax Benefits: How Husband and Wife Can Both Save Income Tax

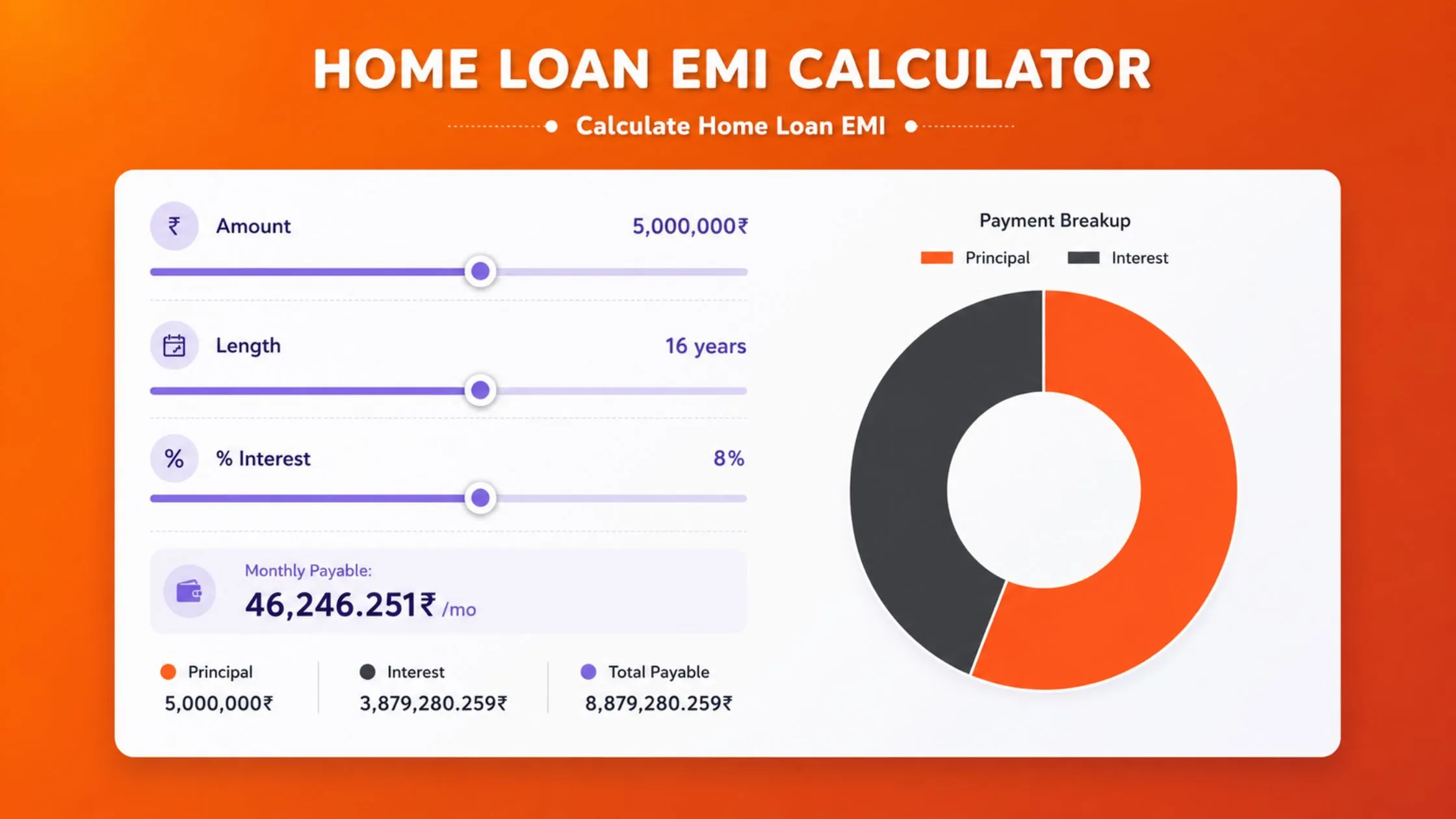

AquireAcres EMI Calculator for Smart Home Loan Balance Transfer Planning

The AquireAcres EMI Calculator is the fastest way to validate whether a home loan balance transfer actually works in your favour before you apply to a single lender. Enter your outstanding loan amount, current interest rate, new offered rate, and remaining tenure to instantly calculate your revised EMI, monthly saving, total interest reduction, and break-even period. Use it before initiating any balance transfer conversation, with your existing lender or a new one.

Red Flags: When a Balance Transfer Will Not Help You

If more than two of the above conditions apply to your current loan situation, than it is probably high time for you to look into options for another strategy.

- Rate difference is below 0.5%: Transfer costs will exceed savings over any break-even horizon

- Tenure has less than 7 years remaining: Interest component is minimal now; the switch delivers no real gain

- CIBIL score is below 700: Expect rejection or a rate that eliminates the savings entirely

- Delayed EMI or active default on record: No lender approves a transfer with compromised repayment history

- New lender's processing fee exceeds 1%: Negotiate this before signing; it cuts into your break-even directly

Conclusion

The home loan balance transfer requires evaluation of financial numbers which show their impact during the rest of the loan period. The current year presents its most significant financial decision when you have a substantial outstanding principal and early-to-mid repayment stage and your interest rates show a meaningful difference. You should perform break-even analysis by examining three different lenders and then proceed after you reach a definite conclusion about the financial outcomes.

Ans 1. A home loan balance transfer shifts your outstanding loan to a new lender offering a lower interest rate, reducing your monthly EMI and total interest paid over the remaining tenure.

Ans 2. On ₹40 lakh outstanding, a 1.25% rate cut lowers EMI by ₹2,500–₹2,700 monthly and saves ₹5–6 lakhs in total interest over 18 years. Savings depend on outstanding principal and the rate differential.

Ans 3. A CIBIL score of 725 or above is the standard approval threshold. Scores below 700 typically result in rejection or a rate offer that eliminates the financial benefit entirely.

Ans 4. No. Expect a processing fee of 0.5%–1%, legal charges of ₹5,000–₹15,000, and stamp duty. Floating rate borrowers pay zero foreclosure charges to the old lender per RBI guidelines.

Ans 5. You need an NOC and Foreclosure Letter from your current lender, KYC documents, income proof (salary slips or ITR), and property documents including title deeds and approved building plan.

Ans 6. The No Objection Certificate is a mandatory legal document from your current lender confirming no objection to transferring your outstanding loan to a new financial institution.

Ans 7. Yes. Most lenders allow a top-up loan above the transferred amount at rates lower than personal loans, processed simultaneously with the transfer, ideal for home renovation needs.

Ans 8. Avoid if the rate difference is below 0.5%, tenure has under 7 years remaining, CIBIL score is below 700, there is a delayed EMI record, or you plan to prepay fully within 12 months.

Ans 9. Most lenders require a minimum of 12 EMIs paid with the current lender before accepting a balance transfer application. Some require up to 18 months of clean repayment history.

Ans 10. The transfer typically completes in 10–15 working days after full document submission. The Foreclosure Letter from the old lender takes approximately 15 working days to process and issue.