✦ AI Summary

Table of Content

▲- What Is the 50-30-20 Rule for Home Loans?

- Applying the Rule: A Real Tier 2 City Example

- Tier 2 City vs Metro: How the Numbers Compare

- How to Allocate Your 20% Savings Bucket

- Red Flags: When the EMI Is Breaking the Rule

- AquireAcres EMI Calculator for Smart Home Loan Planning

- 5 Practical Rules Before You Budget Your EMI

- Conclusion

The 50-30-20 Rule for Home Loans is the most actionable personal finance framework for salaried homebuyers managing a home loan EMI in a Tier 2 city today. The rule divides your monthly take-home income into three non-negotiable buckets, which allocate 50% for needs that include your EMI, 30% for wants, and 20% for savings. The rule is fully attainable for buyers who live in Indore, Jaipur, Lucknow, Nagpur, and Coimbatore because their property prices range between ₹35 lakh and ₹55 lakh and their household expenses remain below metro costs.

Ignoring this structure after taking a home loan is where most Tier 2 city buyers go wrong. They prioritize the EMI, forget the savings bucket, and end up cash-strapped within 18 months of possession. This guide breaks down every parameter, EMI-to-income ratio, savings allocation, real-salary example, and red flag so you manage your home loan without sacrificing financial security.

What Is the 50-30-20 Rule for Home Loans?

The rule allocates your monthly take-home salary as follows:

- 50% Needs: Home loan EMI, groceries, school fees, utilities, health insurance, transport

- 30% Wants: Dining out, OTT subscriptions, travel, shopping, hobbies, gadgets

- 20% Savings: SIP, PPF, emergency fund, term insurance premium, annual loan prepayment

When applied to home loan management, your EMI must sit within the 50% Needs bucket and not dominate it. Financial advisors across India recommend that a home loan EMI should not exceed 35–40% of monthly take-home income. In Tier 2 cities, where average loan sizes sit between ₹25 lakh and ₹55 lakh, hitting this benchmark is far more realistic than in any metro.

Applying the Rule: A Real Tier 2 City Example

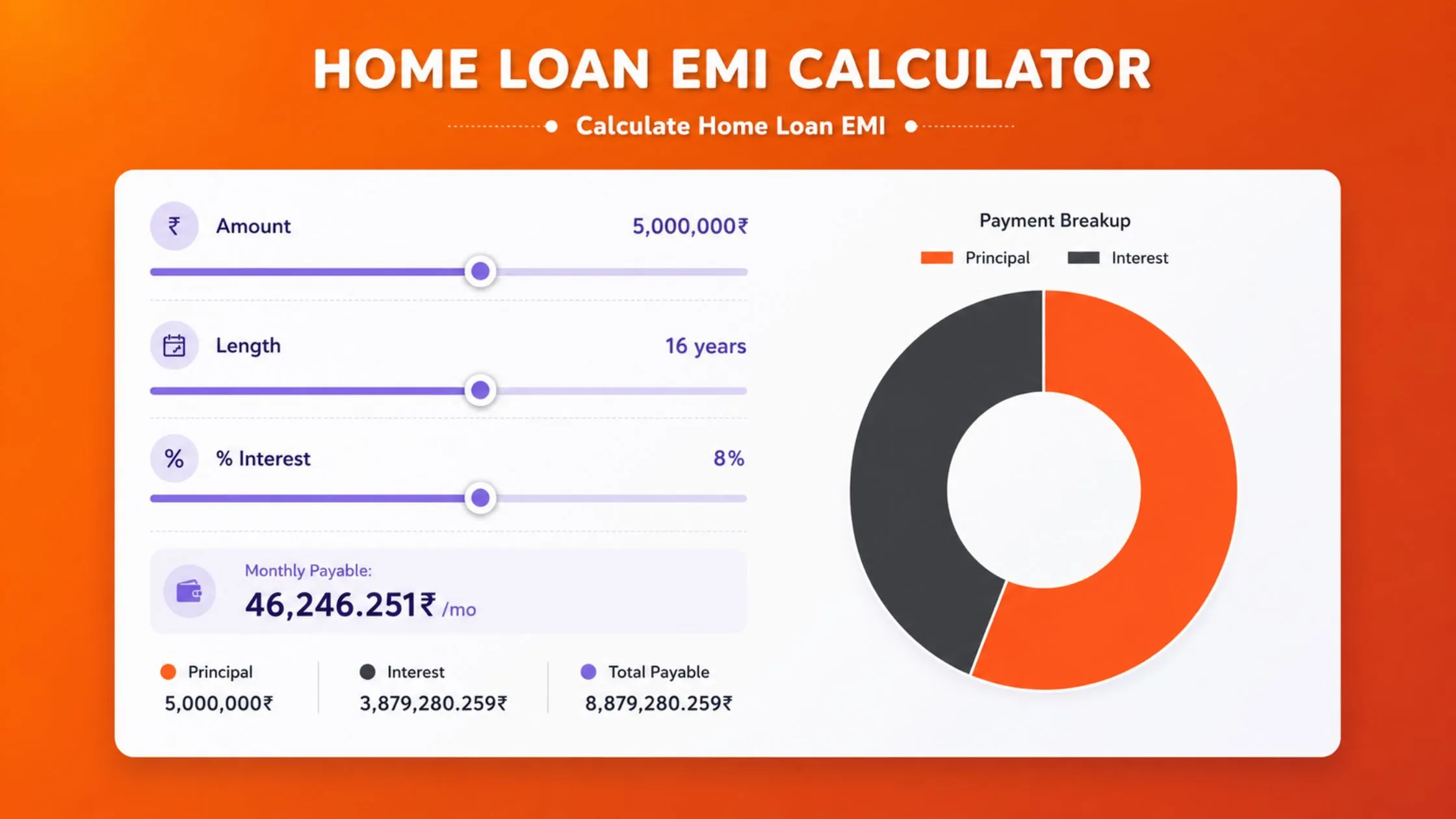

The rule shows its effects through Priya's situation who works as an IT professional in Indore and earns ₹75,000 every month while she pays ₹22,000 for her home loan, which consists of a ₹40 lakh loan at 8.6% interest for a period of 20 years.

|

Budget Bucket |

Allocation |

Monthly Amount |

What It Covers |

|---|---|---|---|

|

Needs |

50% |

₹37,500 |

EMI ₹22,000 + groceries, utilities, transport, school fees |

|

Wants |

30% |

₹22,500 |

Dining, travel, OTT, shopping, hobbies |

|

Savings |

20% |

₹15,000 |

SIP ₹6,000 + PPF ₹3,000 + emergency fund ₹3,000 + prepayment ₹3,000 |

What the numbers actually mean: Priya's EMI at ₹22,000 consumes 29% of income, well within the safe zone. Her Needs bucket still has ₹15,500 for all essential household expenses. The Savings bucket at ₹15,000 covers both investments and a prepayment fund. This is what a balanced Tier 2 home loan budget looks like.

Also Read: Fixed vs. Floating Interest Rate: A 20-Year Cost Breakdown for 2026

Tier 2 City vs Metro: How the Numbers Compare

The 50-30-20 rule debate reaches its practical application when people start to calculate paisa and rupees. The structural affordability gap between Tier 2 cities and metros exists at a level that determines whether the rule functions properly or becomes completely unworkable.

|

Parameter |

Tier 2 City |

Metro (Mumbai/Delhi) |

|---|---|---|

|

Average property price |

₹35–55 lakh |

₹90 lakh–₹2 crore |

|

Typical home loan EMI |

₹25,000–₹40,000 |

₹65,000–₹1,40,000 |

|

Monthly household expenses |

₹12,000–₹18,000 |

₹30,000–₹55,000 |

|

Income needed to apply the rule |

₹60,000–₹90,000 |

₹1,80,000–₹3,00,000 |

|

EMI-to-income ratio feasibility |

High |

Low to Moderate |

|

Dining out cost (2 people) |

₹800–₹1,200 |

₹2,500–₹4,000 |

What the numbers actually mean: A salaried professional earning ₹75,000/month in Indore can comfortably follow the 50-30-20 rule with a ₹40-lakh home loan. Mumbai residents with the same earnings face difficulties because their home loan EMI costs exceed their income, which prevents them from saving 20% of their earnings. The framework operates more effectively in Tier 2 cities because these cities possess better structural foundations for its implementation.

How to Allocate Your 20% Savings Bucket

The biggest mistake Tier 2 city homebuyers make is treating the EMI as the only financial obligation post-purchase. The 20% savings bucket is what separates financially secure homeowners from those who are one expense away from crisis. Here is the recommended split within the 20% bucket:

- SIP in equity mutual funds or ELSS: 6–8% of income. Qualifies for deduction under Section 80C. Targets 10–14% CAGR over the long term.

- PPF or NPS contributions: 3–4% of income. Tax-efficient, long-term wealth building under Section 80C.

- Emergency fund top-up: 3–4% of income until 6 months of total expenses are covered in a liquid instrument.

- Annual home loan prepayment kitty: 2–3% of income. Deployed as a lump-sum once a year to cut principal.

- Term and health insurance premiums: 1–2% of income. Non-negotiable protection layer for a home loan borrower.

Why prepayment matters: The total interest payments on a ₹40-lakh loan at 8.6% interest over 20 years period will exceed the principal amount by approximately ₹44 lakh. The total duration of the loan decreases by 18 to 24 months when customers make annual lump-sum payments between ₹40,000 and ₹50,000 which also results in interest savings of several lakhs.

Also Read: How Much Home Loan Can You Really Get on a 25,000 Monthly Salary?

Red Flags: When the EMI Is Breaking the Rule

It is important to work on increasing your financial security when at least two of the situations mentioned below explain your situation today.

- EMI exceeds 40–45% of monthly take-home: The Needs bucket is already overrun before groceries are budgeted

- SIP contributions have stopped: The savings bucket has been effectively zeroed out by the EMI pressure

- Credit card use for groceries by month-end: A clear sign that the 50% Needs cap has been breached in practice

- No emergency fund covering 3 months: Any job disruption or medical expense will force a loan default

- Society maintenance not budgeted: There exists no budget for maintaining the society because the Tier 2 apartment maintenance expenses which range from ₹2,000 to ₹8,000 per month, should be included in pre-purchase assessments yet they remain unrecognized.

- Wants spending is near zero: People spend almost nothing because they need to maintain a 30 percent buffer for their budget which proves to be unmanageable according to their present financial situation.

AquireAcres EMI Calculator for Smart Home Loan Planning

The AquireAcres EMI Calculator is the fastest way to apply the 50-30-20 rule to your specific loan amount, salary, and tenure. Enter your take-home salary, expected loan amount, and interest rate to instantly see whether your EMI fits within the 50% Needs ceiling, and how much is left for savings and lifestyle. Use it before finalising any home loan offer.

5 Practical Rules Before You Budget Your EMI

- Your first tip says keep EMI below 40% of your salary, but your second tip allows spending over 50% on needs like groceries, bills, school, and transport. If all 50% goes to EMI, nothing is left for basic needs. The safe EMI range is 35%–40% of your income.

- Tax deductions should be used to determine your actual EMI expenses. Section 24(b) provides an annual interest deduction of ₹2 lakh for taxpayers. Section 80C allows taxpayers to deduct ₹1.5 lakh in principal repayments. The 20% tax bracket borrower experiences a reduction in monthly EMI payments between ₹500 and ₹1,500.

- Your budget calculations should include EMI payments with an additional 1 percentage point interest rate increase. The Needs bucket calculations require you to use the existing EMI payment and the higher rate which is 1% more than that. Your EMI payments for a 40-lakh floating-rate loan will increase between ₹1,500 and ₹3,000 per month whenever the RBI raises interest rates.

- Step-up EMI plans start lower and increase 5–10% annually with salary growth. The Needs bucket functions for early years while the Savings bucket expands according to your income growth.

- A top-up loan should never be used to pay for your personal expenses. Top-up loans become more attractive after you make a purchase but they increase your monthly payments which lead to higher spending than 50% and destroy your entire 50-30-20 financial plan. You should only use top-up loans for home renovation purposes.

Conclusion

The choice of how to manage a home loan comes down to one decision: whether your EMI serves your financial life or dominates it. The 50-30-20 Rule for Home Loans gives every Tier 2 city homebuyer a clear, data-backed answer. Keep EMI within the 50% Needs boundary, protect the 20% savings allocation without compromise, and let the 30% Wants bucket give you a life worth living inside your new home. In Tier 2 cities, where affordability is real and financial discipline is achievable, this rule is not just a framework, it is your blueprint for building equity without burning out.

Ans 1. The 50-30-20 rule for home loans is a budgeting framework that divides monthly take-home income into three buckets, 50% for Needs (including your EMI), 30% for Wants, and 20% for Savings. It ensures your home loan EMI is managed within a sustainable financial structure without sacrificing savings or lifestyle spending.

Ans 2. Financial advisors in India recommend that a home loan EMI should not exceed 35–40% of monthly take-home salary. Including all EMIs combined (home loan, car loan, personal loan), total debt obligations should stay within 50% of income, the Needs ceiling in the 50-30-20 rule.

Ans 3. Yes, the 50-30-20 rule is more practical in Tier 2 cities than in metros. Lower property prices (₹35–55 lakh vs ₹90 lakh+ in metros), smaller EMIs, and a lower cost of living make it significantly easier to keep EMI within the 50% Needs bucket while protecting the 20% savings allocation.

Ans 4. On a ₹60,000 monthly take-home salary, your EMI should ideally not exceed ₹21,000–₹24,000 (35–40% of income). This corresponds to an eligible home loan amount of approximately ₹20–₹25 lakh at 8.5–9% over 20 years, well-suited for Tier 2 city properties in the ₹25–₹35 lakh bracket.

Ans 5. Both have a place in the 20% savings bucket. Allocate 6–8% of income to SIP (targeting 10–14% CAGR in equity funds) and 2–3% to an annual prepayment kitty. Prepayment offers a guaranteed return equal to your loan rate (~8.5–9%), while SIP targets higher long-term growth. Neither should be skipped.

Ans 6. The 50% Needs bucket includes all essential, non-discretionary expenses, your home loan EMI, grocery and food costs, utility bills, school or college fees, health insurance premiums, and commuting costs. In Tier 2 cities, all of these combined typically total ₹30,000–₹45,000/month on a ₹60,000–₹90,000 salary.

Ans 7. Section 24(b) allows a deduction of up to ₹2 lakh per year on home loan interest. Section 80C permits deduction of up to ₹1.5 lakh on principal repayment. For a borrower in the 20% tax bracket, this translates to annual tax savings of up to ₹70,000, effectively reducing the net monthly EMI cost by ₹500–₹1,500.

Ans 8. A step-up EMI plan allows borrowers to start with a lower monthly EMI and increase it by 5–10% annually as salary grows. This keeps the Needs bucket well within 50% in the early loan years and is ideal for salaried professionals aged 28–38 in Tier 2 cities who expect regular income growth.

Ans 9. Key red flags include: EMI exceeding 40–45% of monthly take-home, SIP contributions stopped post-purchase, using credit cards for groceries by month-end, no emergency fund covering 3 months of expenses, and zero discretionary spending left in the budget. Any two of these signals warrant immediate loan restructuring or a prepayment strategy review.

Ans 10. Yes. The AquireAcres EMI Calculator allows you to enter your loan amount, interest rate, and tenure to instantly calculate your monthly EMI. You can then cross-check whether the EMI falls within 35–40% of your take-home salary to validate alignment with the 50-30-20 rule before finalising your home loan.