✦ AI Summary

Table of Content

▲- Understanding Home Loan Eligibility on ₹25,000 Salary

- How Much Home Loan Can You Actually Get?

- Key Factors That Decide Your Loan Eligibility

- EMI vs Loan Amount Comparison Table

- What Kind of Property Can You Afford?

- Smart Strategies to Increase Your Loan Eligibility

- Documents Required for Home Loan Approval

- Common Mistakes to Avoid

- Expert Tip for ₹25,000 Salary Buyers

- Conclusion

Buying a home on a ₹25,000 salary may sound difficult but it remains an achievable goal. The key lies in understanding how banks calculate your eligibility for home loan and how much EMI you can realistically afford and how smart financial planning helps you increase your loan amount. Let us explain the process through a basic practical demonstration.

Understanding Home Loan Eligibility on ₹25,000 Salary

Banks and housing finance companies don't approve loans based on salary alone. What they're actually evaluating is how much monthly repayment you can comfortably handle without putting your basic finances under strain.

Most lenders follow a standard rule:

- EMI should not exceed 40%–50% of your monthly income

So, if your salary is ₹25,000:

- Safe EMI range: ₹10,000 per month

- Stretch EMI range: ₹10,000 to ₹12,500

Going beyond this can increase financial risk and reduce your monthly savings.

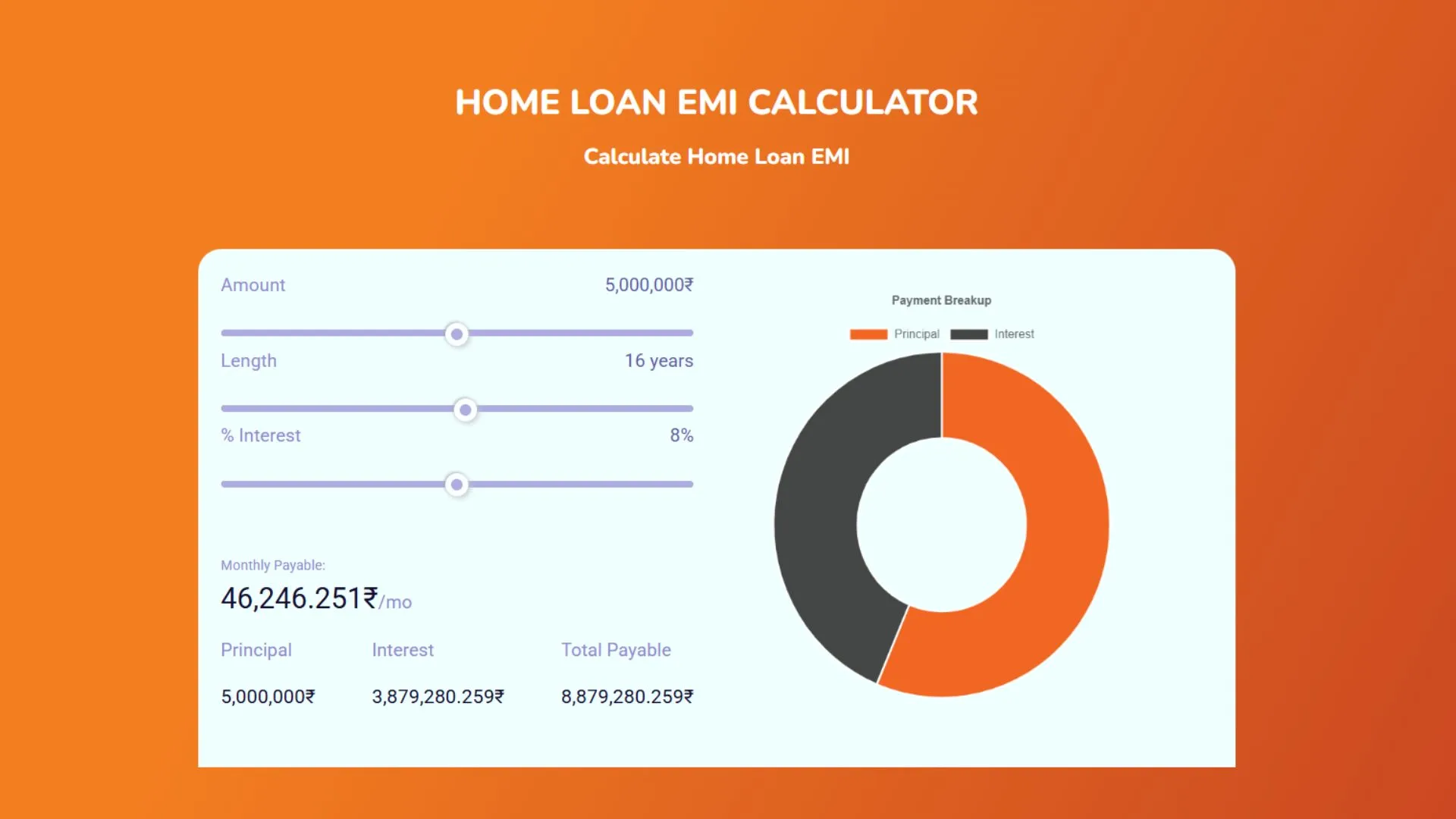

To know the monthly EMI you have to pay according to your loan sanctioned you can calculate by using EMI calculator.

Also Read: Step-Up EMI: How It Works and Who Can Benefit from It

How Much Home Loan Can You Actually Get?

The loan amount a bank offers is directly tied to three variables: how much EMI you can pay, how long your repayment tenure is, and what interest rate applies to your profile. At current market rates of approximately 8% to 9%

Realistic Loan Estimates

Based on current interest rates (~8%–9%):

- ₹10,000 EMI can fetch approx:

- ₹8 lakh (10 years)

- ₹10 lakh (15 years)

- ₹11.5 lakh (20 years)

- ₹13 lakh (30 years)

Some lenders may offer higher amounts (up to ₹17–20 lakh), but that usually depends on:

- Co-applicant income

- Higher tenure

- Strong credit profile

Reality check: For a basic salary of ₹25,000, a separate loan sanction mostly ranges from ₹10 lakh to nearly ₹15 lakh.

Key Factors That Decide Your Loan Eligibility

Even with the same salary, two people can get different loan amounts. Here’s why:

1. FOIR (Fixed Obligation to Income Ratio)

FOIR measures what percentage of your monthly income is already committed to existing loan EMIs, credit card minimum payments, or other fixed obligations.

- Ideally kept below 40%–50%

- Higher existing EMIs = lower eligibility

2. Credit Score

Your CIBIL score tells lenders how reliably you've managed borrowed money in the past.

- 750+ score better chances and lower interest

- Poor score lower loan approval or higher rates

3. Job Stability

Frequent job changes, employment gaps, or contractual work without a formal salary structure can reduce the loan amount a bank is willing to sanction.

- Minimum 2–3 years of consistent job history preferred

4. Age and Loan Tenure

Younger applicants have a natural advantage, a 28-year-old can access a 30-year loan tenure, which spreads repayment across more months and increases the total amount sanctioned for the same EMI.

- Younger applicants get longer tenure and higher loan amount

5. Down Payment Capacity

A larger down payment reduces the loan required, lowers your EMI, and often improves the lender's confidence in your financial discipline.

- Banks finance 75%–90% of property value

- You must arrange the rest

EMI vs Loan Amount Comparison Table

|

Loan Tenure |

EMI (Approx) |

Loan Amount (₹) |

Suitability |

|

10 Years |

₹10,000 |

₹8 lakh |

Low interest, high EMI pressure |

|

15 Years |

₹10,000 |

₹10 lakh |

Balanced option |

|

20 Years |

₹10,000 |

₹11.5 lakh |

Most practical |

|

25–30 Years |

₹10,000 |

₹12–13 lakh |

Higher eligibility, more interest |

Longer tenure = higher loan eligibility but more total interest paid.

Also Read: How Much Home Loan Can I Get on ₹60,000 Salary in India?

What Kind of Property Can You Afford?

Converting loan figures into tangible property choices is where reality sets in. Here’s a realistic affordability example:

- Loan: ₹12 lakh

- Down payment (20%): ₹3 lakh

- Total property budget: ₹15 lakh

Best Options for This Budget:

- Cost-effective housing initiatives in Tier 2 and Tier 3 urban areas such as the outskirts of Lucknow, the periphery of Nagpur, developing zones in Jaipur, or smaller towns where real estate costs are significantly lower

- Properties accessible through government initiatives such as Pradhan Mantri Awas Yojana provide interest subsidies that significantly enhance your financial capability

- Locations on the outskirts of major metropolitan areas, 30 to 50 km from downtown, where land prices are more affordable and connectivity is enhancing

Metro cities like Delhi, Mumbai, or Bangalore may be challenging without a co-applicant.

Smart Strategies to Increase Your Loan Eligibility

If ₹10–12 lakh feels low, here’s how you can boost it:

- Adding a co-applicant – a working spouse, parent, or sibling whose income combines with yours can significantly raise the eligible loan amount, mostly by 50% or more

- Improve your credit score – maintaining timely payments on all bills for 6 to 12 months and reducing credit card usage can elevate a 680 score to over 750, affecting both approval chances and interest rates

- Opt for a longer tenure – extending from 15 to 25 years raises the loan amount possible for the same EMI, although the overall interest paid rises.

- Clear existing loans before applying – reducing your FOIR by paying off a personal loan or vehicle loan before applying gives your home loan application significantly more acceptance.

- Show additional income sources – rental income, freelance work, or agricultural income that can be formally documented may be considered by some lenders.

- Choose an under-construction property for flexibility – some lenders have more flexibility with under-construction projects, and staggered disbursements can ease the immediate financial pressure.

These strategies can increase your loan eligibility by 20%–50% in many cases.

Documents Required for Home Loan Approval

Preparing your documents before approaching a lender will help your application process move faster while showing the bank your ability to organize documents for borrowing needs, which banks consider more important than most borrowers understand.

- Salary slips (last 3–6 months)

- Bank statements

- PAN and Aadhaar

- Employment proof

- Property documents

Proper documentation improves approval chances and speeds up processing.

Common Mistakes to Avoid

Many buyers reduce their chances unknowingly. Avoid these:

- Taking EMI above 50% of salary

- Ignoring credit score before applying

- Not planning for down payment

- Choosing short tenure unnecessarily

- Applying to multiple lenders without research

Expert Tip for ₹25,000 Salary Buyers

If you’re serious about buying a home, the most practical approach for someone at this income level isn't to maximise the loan amount, it's to build a sustainable plan around a manageable EMI.

- Start with a clear EMI plan (₹10,000 max)

- Look for properties under ₹15–20 lakh range

- Consider joint ownership for higher eligibility

- Focus on long-term affordability, not maximum loan

Conclusion

People who earn a monthly salary of ₹25,000 can opt for home loans between ₹10 lakh and ₹13 lakh based on their financial situation and the tenure of loan repayment. Higher loan amounts are available but they bring greater financial risk or need additional applicants for approval.

The smartest approach is not to chase the highest loan but to select a loan amount which leads to affordable monthly payments and stable financial conditions and lifelong financial stability. The right strategy enables people to achieve homeownership through their entire life.

Ans 1. On a ₹25,000 monthly salary, most banks will sanction a home loan between ₹10 lakh and ₹13 lakh, depending on your tenure, credit score, and existing financial obligations. With a co-applicant or strong credit profile, some lenders may approve up to ₹15 to ₹17 lakh.

Ans 2. The recommended maximum EMI on a ₹25,000 salary is ₹10,000 to ₹12,500 per month — which represents 40% to 50% of monthly take-home pay. Staying within this range ensures financial stability while managing home loan repayments.

Ans 3. Most public sector banks including SBI, Bank of Baroda, and PNB, as well as housing finance companies like LIC HFL and HDFC Ltd, offer home loans to applicants earning ₹25,000 per month. Terms vary, and comparing offers across at least 3 to 4 lenders is advisable.

Ans 4. A ₹20 lakh loan on a ₹25,000 salary is difficult on a standalone basis, as the resulting EMI would exceed the safe repayment threshold. It becomes more achievable with a co-applicant, a very high credit score, and a 25 to 30-year tenure.

Ans 5. Yes, significantly. A CIBIL score of 750 or above improves both your approval chances and the interest rate offered, which directly affects how much loan you can access for the same EMI. A poor score can result in rejection or rates that substantially increase your total repayment.

Ans 6. Yes, individual applications are accepted. However, the sanctioned amount is typically limited to ₹10 to ₹13 lakh. Adding a co-applicant with additional income is the most effective way to increase the eligible loan amount significantly.

Ans 7. FOIR (Fixed Obligation to Income Ratio) measures what percentage of your monthly income is already committed to existing EMIs and fixed payments. Lenders prefer FOIR below 50%. If you already have a vehicle or personal loan running, it reduces the home loan EMI capacity available to you and lowers the amount a bank will sanction.

Ans 8. If your annual household income is below ₹6 lakh, you may qualify under the Low Income Group (LIG) category of PMAY, which offers an interest subsidy of up to ₹2.67 lakh on your home loan. This effectively reduces your total repayment burden and improves overall affordability.

Ans 9. The most effective steps include adding a working co-applicant, improving your CIBIL score before applying, clearing existing loans to reduce FOIR, opting for a longer repayment tenure, and documenting any additional income sources that lenders may consider.

Ans 10. Yes. Each loan application triggers a hard enquiry on your credit report, and multiple enquiries in a short period signal financial desperation to lenders which can lower your score and reduce approval chances. Research and compare lenders first, then apply to one or two selectively.