✦ AI Summary

Table of Content

▲- What Happens the Moment You Miss an EMI?

- How a Missed EMI Escalates: The Cost Timeline

- ECS Penalty vs. Penal Interest: Know the Difference

- Common Reasons for EMI Bounce and Prevention

- Immediate Steps If You've Already Missed an EMI

- AquireAcres EMI Calculator for Smart Home Loan Planning

- Long-Term Habits to Protect Your CIBIL Score

- Facing a Prolonged Financial Crisis?

- Conclusion

A home loan EMI payment that a borrower fails to make establishes the most severe financial damage that a salaried homebuyer can face because it results in ECS bounce fees and accumulates penalty interest and leads to a CIBIL score reduction which lasts for seven years. The payment consequences start to occur within hours after a payment deadline passes and they become worse with every unpaid day that follows.

Most borrowers who miss an EMI make one critical mistake that they wait. They assume a single bounce is a minor inconvenience. It is not. Banks start the DPD (Days Past Due) clock from day one, credit bureaus receive updated data within 30–45 days, and penal interest compounds daily. Understanding the complete mechanism and acting before the monthly reporting cycle runs, is what separates borrowers who recover in weeks from those who spend years repairing their credit profile.

What Happens the Moment You Miss an EMI?

The instant your ECS/NACH auto-debit fails, three simultaneous financial events are triggered:

- ECS/NACH Return Charge: Your bank levies ₹300–₹750 + GST for the failed debit, sometimes charged on both the savings account and the loan account.

- Penal Interest: The lender applies 1%–3% per month on the overdue amount, calculated and compounding daily until full repayment.

- CIBIL Reporting Risk: Banks submit repayment data to credit bureaus monthly. If your EMI is unpaid at the reporting cycle, a DPD entry is flagged, and one 30-DPD mark can cut your CIBIL score by 50–100 points.

How a Missed EMI Escalates: The Cost Timeline

|

Timeline |

Loan Classification |

CIBIL Score Impact |

Next Risk |

|

0–30 Days |

SMA-0 (Special Mention) |

50–80 point drop |

DPD entry at reporting cycle |

|

31–60 Days |

SMA-1 |

80–120 point drop |

Legal notice warning |

|

61–90 Days |

SMA-2 |

Severe, 120–150 pts |

Formal recovery proceedings |

|

90+ Days |

NPA (Non-Performing Asset) |

150–200+ pts, stays 7 years |

SARFAESI action possible |

If a borrower just ignores one bounce for 90 days, then a fixable ₹300–₹750 kind of penalty basically turns into an NPA tag, and it blocks eligibility for another loan for years. All that harm is mostly avoidable though, if you take action within the first 48 hours, like right away.

ECS Penalty vs. Penal Interest: Know the Difference

|

Charge Type |

Levied By |

Amount |

Trigger Point |

|

ECS/NACH Return Charge |

Your bank |

₹300–₹750 + GST |

On the bounce date itself |

|

Penal Interest |

The lender |

1%–3% per month on dues |

Runs daily until repayment |

|

Late Payment Fee |

Some lenders |

Fixed % of EMI amount |

After grace period ends |

On a ₹35,000 EMI, that 2% per month penal interest , running roughly for 45 days ends up adding about ₹1,050 in extra charges, over and above the bounce fee. Each day of delay is this measurable and very avoidable cost, not some minor thing.

Also Read: Step-Up EMI: How It Works and Who Can Benefit from It

Common Reasons for EMI Bounce and Prevention

- Low account balance on due date; Maintain a standing buffer of 1.5× your EMI amount in the linked account at all times.

- If your salary got credited late, you should contact your lender proactively before the due date, not after, so you can request a short grace window.

- NACH mandate is expired or just not matching, double-check that the mandate is still active every year, because the renewal takes about 15–30 days, so start the process early.

- Bank account change not updated: New account? Update the ECS instruction at least 30 days before your next EMI date.

- No reminder system: Set recurring calendar alerts 3–4 days before the EMI date every month without exception.

Immediate Steps If You've Already Missed an EMI

Act within 24–48 hours. Every additional day compounds penal charges and brings the monthly reporting cycle closer.

- Top up and repay immediately: Fund the account and trigger a manual transfer the same day if the bounce was due to low balance.

- Call your lender proactively: Request a waiver on ECS bounce charges, first-time defaulters with a clean repayment history frequently receive this.

- Request nil DPD reporting in writing: If you clear the dues before the bank's monthly reporting cycle, formally ask for '0 DPD' reporting for that month.

- Save all payment proof: SMS confirmation, bank receipt, and email acknowledgement, all with the exact clearance date.

- Verify your CIBIL report after 45–60 days: Log in to cibil.com and confirm the DPD column reads '000' for the concerned month.

Red Flags: Your EMI Situation Needs Immediate Attention if

- EMI exceeds 40–45% of your monthly take-home salary

- SIP or recurring deposits have been stopped to keep up with EMI

- You use a credit card for groceries in the last week of the month

- No emergency fund covering at least 3 months of total expenses

- Two or more bounce notifications received in the past 6 months

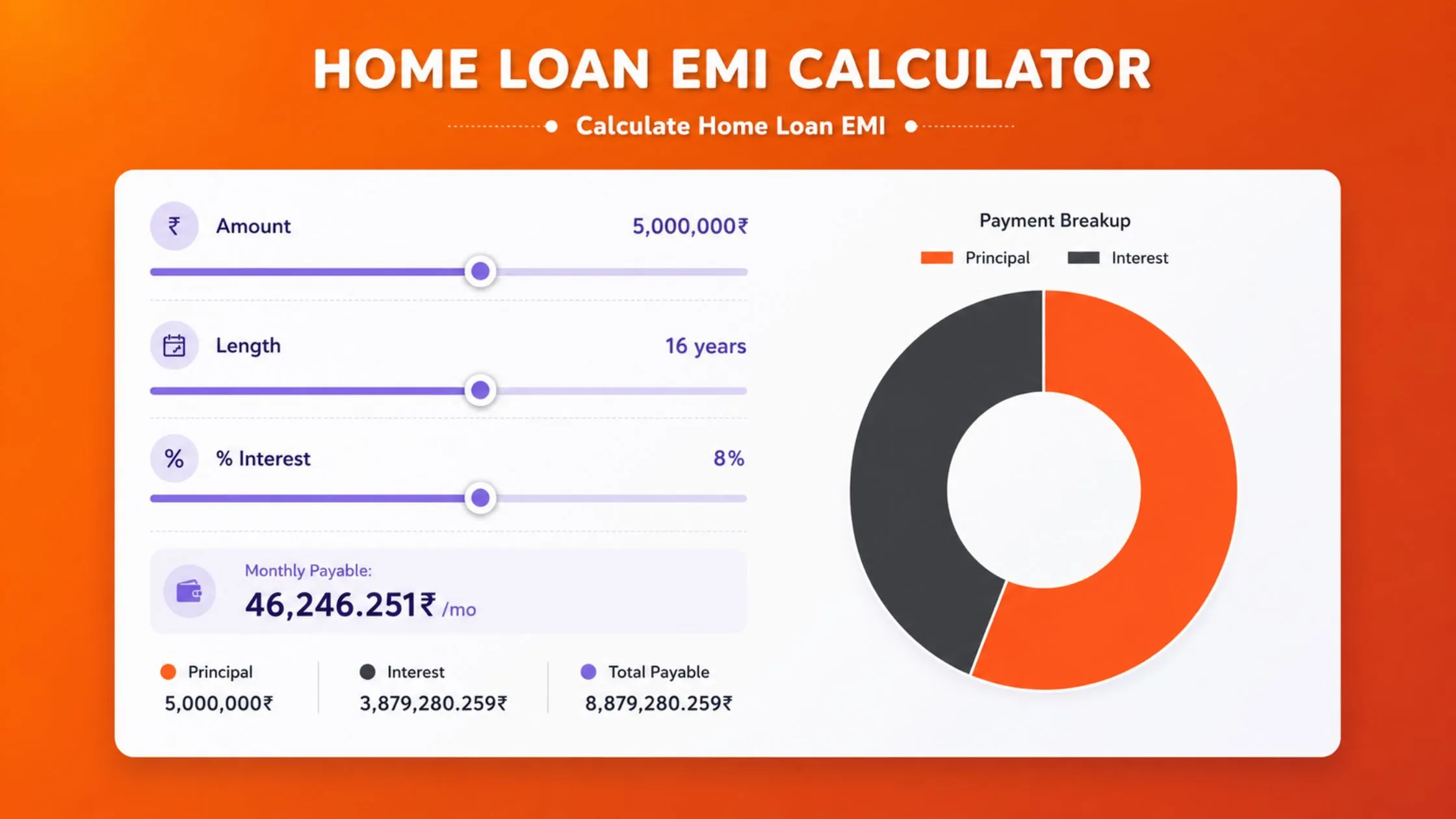

AquireAcres EMI Calculator for Smart Home Loan Planning

Use the AquireAcres EMI Calculator to check whether your home loan EMI fits within the safe 35–40% income ceiling before you commit to any loan offer.

Also Read: Joint Home Loan Tax Benefits: How Husband and Wife Can Both Save Income Tax

Long-Term Habits to Protect Your CIBIL Score

- Build a dedicated EMI reserve account: Park 2–3 months of EMI amounts in a separate savings account, never touch it for anything else.

- Align EMI debit with salary credit: Set your NACH debit 2–3 days after your typical salary credit date to eliminate most bounce scenarios permanently.

- Add a standing instruction as backup: Runs in parallel with NACH and activates automatically if the primary debit fails.

- Prepay annually when surplus is available: If you can prepay yearly when there is surplus money. Like a ₹40,000–₹50,000 lump sum prepayment done annually will trim about 18–24 months from a 20-year loan tenure.

- Monitor CIBIL quarterly: Free checks are available on Paisabazaar and BankBazaar. Errors caught early can be disputed and corrected within 30 days under RBI norms.

Facing a Prolonged Financial Crisis?

- Loan restructuring, according to RBI guidelines banks are expected to provide a proper structured resolution for borrowers who are genuinely stressed , often by doing tenure extension so the monthly outflow eases a bit.

- EMI moratorium in case of documented hardship (like job loss , or a medical emergency) , lenders could agree to give you a 1–3 month breather or pause on your EMI payments . Interest accrues, but no DPD is reported during the approved period.

- Balance Transfer basically means you move to a lender that offers interest which is maybe 0.5% lower, on a ₹40 lakh loan, and that shift saves about ₹1.5–₹2 lakh across the whole tenure, plus it actually reduces your monthly EMI, so it feels simpler month to month.

- RBI credit counselling , through RBI empanelled centres , offers free guidance that helps you form a more systematic repayment strategy which banks will accept,all while it costs nothing to you as the borrower.

Conclusion

A missed home loan EMI does not have to define your financial future, but only if you respond with speed and precision. The combination of same-day repayment, proactive lender communication, a written request for nil DPD reporting, and quarterly CIBIL monitoring is what protects both your credit score and your homeownership journey.

Build the right systems, the EMI buffer account, the aligned auto-debit date, and the annual prepayment habit before a crisis ever strikes. Your home is your most valuable asset; guard it with the financial discipline it demands.

_1784272311.webp)

Ans 1. Missing one home loan EMI immediately triggers an ECS bounce charge of ₹300–₹750 + GST, daily penal interest of 1%–3% per month on the overdue amount, and a potential 30-DPD entry on your CIBIL report if the dues are not cleared before the bank's monthly credit bureau reporting cycle runs.

Ans 2. A single 30-DPD entry can reduce your CIBIL score by 50–80 points. Two consecutive missed EMIs (60 DPD) can cause an 80–120 point drop. NPA classification after 90+ days results in a 150–200+ point decline that remains on your credit report for up to 7 years.

Ans 3. DPD stands for Days Past Due. It indicates how many days a loan payment was overdue at the time of bureau reporting. '000' means the payment was made on time. Any value above 000, such as 030, 060, or 090, indicates a delay and directly and negatively impacts your credit score.

Ans 4. Yes. Banks frequently waive ECS/NACH bounce charges for first-time defaulters who have a clean prior repayment record. You must submit a written request, either to the branch manager or via the bank's official complaint portal, promptly after clearing the overdue EMI.

Ans 5. SMA (Special Mention Account) is an early-warning classification, SMA-0 covers 0–30 days overdue, SMA-1 covers 31–60 days, and SMA-2 covers 61–90 days. NPA (Non-Performing Asset) is declared after 90+ consecutive days of non-payment and carries severe credit damage and potential legal recovery action under the SARFAESI Act.

Ans 6. A DPD entry or NPA classification remains visible on your CIBIL report for up to 7 years from the date of first default, even after full repayment of all dues. This is why immediate action after a bounce is non-negotiable, the record cannot be erased, only prevented.

Ans 7. Yes. If you paid your EMI on time but the bank reported it incorrectly as overdue, file a dispute on the CIBIL Dispute Resolution portal at cibil.com. CIBIL is required to investigate and respond within 30 days under RBI directives. Always attach your payment proof when raising the dispute.

Ans 8. No, a formally sanctioned moratorium does not trigger DPD reporting during the approved period. However, interest continues to accrue and is added to the outstanding principal. Always obtain written confirmation from your lender that the moratorium is officially approved before the EMI due date.

Ans 9. Set your NACH auto-debit 2–3 days after your salary credit date, maintain a 1.5x EMI buffer in the linked account at all times, add a standing instruction as a backup debit mechanism, and verify your NACH mandate validity every year. These four habits eliminate the vast majority of bounce scenarios permanently.

Ans 10. No. A single missed EMI does not give a bank the legal authority to initiate property recovery. Under the SARFAESI Act, a lender can begin proceedings only after the loan account is classified as NPA, which requires 90+ consecutive days of non-payment, followed by formal notices being duly served to the borrower.