In this scenario, you must pay tax on your rental property because the GAV is ₹3,60,000, which exceeds the ₹2,50,000 threshold. However, if the rent is ₹15,000 per month, resulting in a GAV of ₹1,80,000 (₹15,000 x 12), you will not be required to pay rental income tax.

Also Read: GST on Construction 2024: All You Need to Know

GST's Role in Tax on Rental Income

According to the Goods and Services Tax (GST) Act, renting an immovable property is classified as a provision of services. However, not all rental income is subject to GST.

A property is considered a supply of services if it is leased, rented, or licensed to occupy, and therefore, it would attract GST. Any property, whether commercial, industrial, or residential, rented for business purposes, is taxable under the GST Act.

On the other hand, rental income from an immovable property solely rented for residential purposes is exempt from GST. This means properties rented out for living purposes are not subject to GST.

However, properties rented out for business activities are liable to pay 18% GST on the rental income, as renting out a property for business is considered a supply of services under the GST Act.

Income Tax on Rental Income: When Property is Not Taxable

You are exempt from paying tax on rental income in the following scenarios:

- Receiving rent from a farmhouse.

- Income from a local authority.

- Income from an approved scientific research association.

- Income from an educational institute.

- Income from a trade union.

- Property rented for charitable purposes.

- Property income of a political party.

- If you use the property for your own business.

- Self-occupied property.

Rental Income Taxation for NRIs

If you are a Non-Resident Indian (NRI) earning rental income from renting out a property, you must pay taxes under Section 24. The limits and deductions are the same for NRIs as for residents of India. However, in this case, the tenant renting the property is responsible for tax payment. The tenant must deduct 31.2% tax at source (TDS) and deposit it into the NRI's account. The TDS form must be submitted to the tax authorities, and Form 15CA must be filed with the Income Tax Department.

NRIs are subject to double taxation: once in India under Section 24, and again in the country where they reside. To avoid double taxation, it is essential to check if there is a Double Taxation Avoidance Agreement (DTAA) between India and the country of residence. If there is no DTAA, India has the right to tax the NRI's rental income. If a DTAA exists, both countries may tax the income. However, if you live in Bangladesh, Greece, or UAR (Egypt), only India, as the source country, can tax the rental income.

Also Read: Freehold Property vs Leasehold Property - Differences, Benefits, Owner Rights

Process to File Income Tax on Rental Income for NRIs

Follow these steps to file tax on rental income for NRIs:

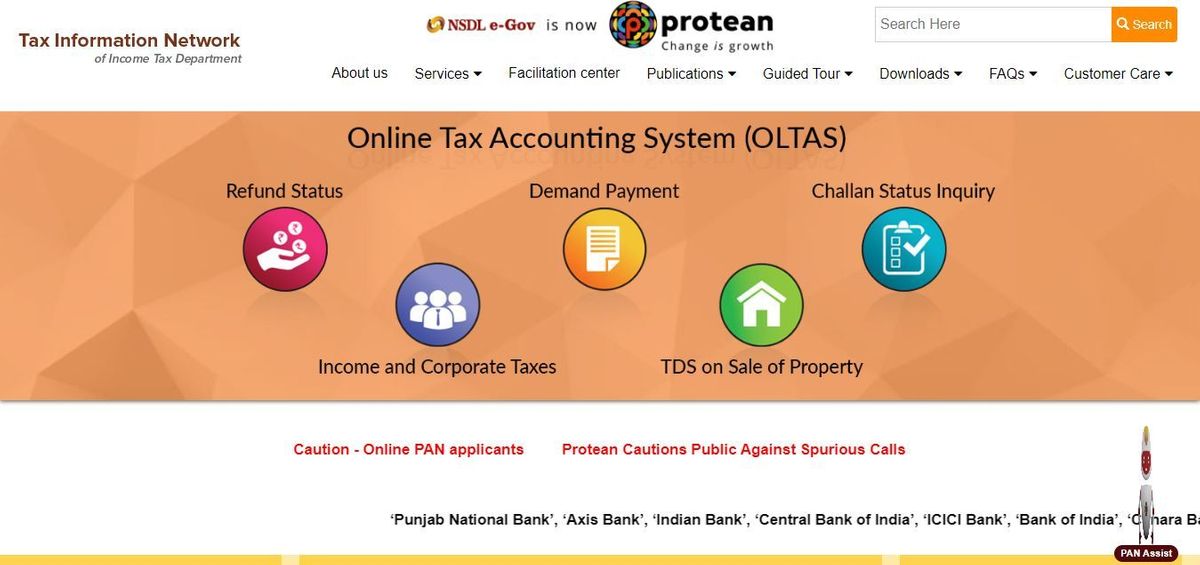

Step 1: Obtain a tax account number (TAN) from the Tax Information Network portal of the Income Tax Department.

- Step 2: Once you have got the TAN number, the tenant should deduct 31.2 percent tax at source and submit that amount to the tax authorities. This amount has to be paid at 7 months of the calendar month. Rest of the amount is paid by the tenant to the property owner.

- Step 3. To make the payment, you should fill in Form 15CA and submit it to the IT department. It is mandatory to pay the taxes on rental income irrespective of the amount.

Tips to Save Tax on Rental Income

You can reduce your tax liability on rental income with the following tips:

- Maintenance Charges: Exclude maintenance charges from the rent received to lower your taxable rental income. For example, if you charge ₹30,000 rent and include ₹5,000 for maintenance, you will be taxed on the full ₹30,000. To avoid this, specify in the rent agreement that maintenance charges are paid directly to the housing society.

- Joint Property Ownership: If you co-own property with a family member (such as a spouse or parent), you can divide the rental income between both of you. This split can reduce the overall tax burden on rental income.

- Municipal Taxes: Deduct municipal taxes like sewage and property tax from your rental income. Ensure these taxes are paid by the property owner, not the tenant. This deduction will lower your taxable rental income and reduce your tax liability.

- Furnished Property: If your property is furnished with additional services (like Wi-Fi, DTH, etc.), ask the tenant to pay these charges separately. This approach will lower your rental income and, consequently, your tax liability.

By applying these strategies, you can effectively manage and potentially reduce your tax on rental income. Remember, Section 24 of the Income Tax Act allows for standard deductions and other ways to save on tax. For charitable trusts, they must claim deductions as capital expenditure during property acquisition, as standard deductions are not available for them.

Income Tax on Rental Income: Charitable Trusts Charitable trusts are not eligible for standard deductions under Section 24(A) for rental income. Instead, they claim capital expenditure deductions at the time of property acquisition, as ruled by the Income Tax Appellate Tribunal in February 2023.

Income Tax on Rental Income: Vacant Houses Previously, if an individual owned multiple properties, only one was considered self-occupied, and the rest were treated as let-out. Since the financial year 2020, property owners can now choose up to two properties as self-occupied, with the remaining properties classified as let-out for tax purposes.

Income Tax on Rental Income: Unrealised Rent Under Section 22 of the Income Tax Act, 70% of rental income is taxable, while 30% is automatically exempt. Unrealised rent, which is rent not collected due to tenant default, can be exempt from tax if the landlord provides satisfactory proof of the tenant's default or eviction. The tax authorities will subtract the unrealised rent from the total taxable rent, easing the financial burden on property owners.

No Tax on Unrealised Rent - ITAT Ruling The Income Tax Appellate Tribunal (ITAT) has ruled that unrealised rent is not subject to tax. This decision benefits property owners dealing with tenants who default on payments or vacate without settling rent, reducing the tax burden.

Tax on Rental Income from REITs Income from Real Estate Investment Trusts (REITs) is generally not taxable if received as dividends. According to the Income Tax Act, 90% of REIT income is taxable and distributed to investors. REITs, similar to mutual funds, invest in commercial real estate, offering potentially high rental returns.

The Bottom Line: Save Tax on Rental Income Understanding and applying rental income tax laws in India can help you save on taxes. Timely tax payments and strategic deductions, such as those available under Section 24(B) for home loan interest, can offer significant benefits. Additionally, co-owning property can further reduce your tax burden.

Also Read: भूमि अतिक्रमण अधिनियम क्या है और संपत्ति या भूमि अतिक्रमण से कैसे निपटें?

Ans 1. You cannot claim a deduction on home loan interest for an under-construction property. It can be claimed only once the construction is finished.

Ans 2. Self-occupied property is where you stay with your family. Let-out property is one that you have given on rent. Deemed let-out is the additional property owned but not occupied by the owner or a tenant.

Ans 3. Paying tax on rental income is mandatory.

Ans 4. Section 24 of the Income Tax Act, 1961, details the deductions that can be availed on rental income.

Ans 5. The owner is supposed to pay the tax on income from housing rent.