✦ AI Summary

Table of Content

▲- What is a Memorandum of Deposit (MOD)?

- How Does MOD Work in a Home Loan?

- Acquire Acres EMI Calculator for Smart EMI’s

- MOD Charges Explained

- MOD Charges vs Other Home Loan Charges

- Factors Affecting MOD Charges

- Benefits of MOD Registration

- Can MOD Charges Be Avoided?

- Common Mistakes Homebuyers Should Avoid

- Conclusion

Buying a home involves more than just arranging the down payment and securing a home loan. Many borrowers focus only on the interest rate and EMI while overlooking several additional charges that come with the loan process. One such cost is the Memorandum of Deposit (MOD) charge, which often surprises first-time homebuyers during loan disbursement.

If you have recently submitted a home loan application or you are planning to apply in 2026, knowing MOD charges can really help you in estimating what the borrowing expense will actually look like. This guide helps you know MOD fees, how they’re determined, why financial institutions tend to impose them, and how these charges can nudge your total home loan costs up or down.

What is a Memorandum of Deposit (MOD)?

When you take a home loan, the lender needs a legally enforceable claim on the property until you've repaid. That claim is created through a mortgage and the Memorandum of Deposit is the legal document that records and formalises that mortgage arrangement.

In practical terms, you hand over your original property title deeds to the bank. The bank creates a MOD that officially documents the fact that these title deeds have been deposited as security for the loan. In many states, this document is registered with the Sub-Registrar's Office, creating a public record of the lender's interest in the property.

The MOD remains valid for the entire loan tenure. When your loan is fully repaid, the bank releases the title deeds and the mortgage is formally discharged, the legal claim on your property ends and full ownership reverts to you without encumbrance.

Why is MOD Required?

The MOD serves multiple purposes:

- Establishes the lender's legal interest in the property

- Creates an official record of the mortgage

- Protects the lender against loan default

- Helps prevent ownership disputes

- Strengthens legal enforceability of the mortgage

Most banks and housing finance companies require MOD registration as part of the home loan process.

Also Read: How to Transfer Your Home Loan to Another Bank for a Lower EMI in 2026

How Does MOD Work in a Home Loan?

When your home loan gets approved the lender asks you to submit the original property documents. After verification, a Memorandum of Deposit is signed and in many states, it’s registered with the appropriate authority. The whole course usually goes something like this:

Step 1: Loan Approval

The bank evaluates your income, creditworthiness, and the property's legal and technical status, and issues a sanction letter confirming the approved loan amount and terms.

Step 2: Deposit of Title Deeds

Submit the original ownership documents of the property to the lender. For properties under construction, the chain of title documents up to the current transaction are deposited. For completed properties, the full ownership documentation is submitted.

Step 3: Creation of MOD

The lender's legal team prepares the Memorandum of Deposit document recording that the title deeds have been deposited as security for the specified loan amount.

Step 4: Registration

In most states, the MOD is registered with the relevant authority, typically the Sub-Registrar's Office. This registration is what creates the public legal record of the mortgage and is what attracts stamp duty and registration charges.

Step 5: Loan Disbursement

Once the MOD formalities are complete, the lender releases the approved loan amount directly to the builder for under-construction properties or through the appropriate payment channel for completed properties.

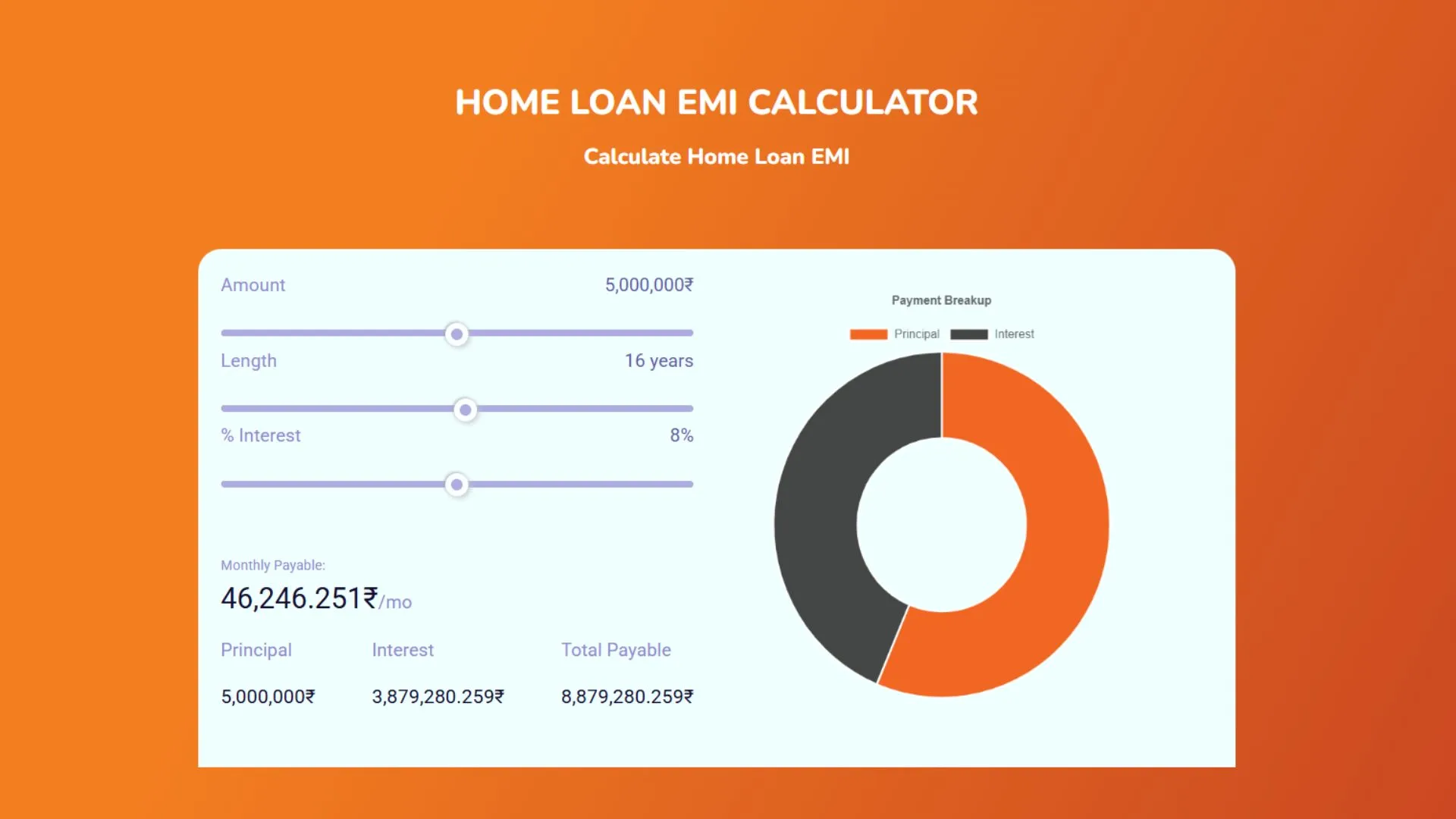

Acquire Acres EMI Calculator for Smart EMI’s

The AquireAcres EMI Calculator is the fastest way to validate whether a home loan balance transfer actually works in your favour before you apply to a single lender. Enter your outstanding loan amount, current interest rate, new offered rate, and remaining tenure to instantly calculate your revised EMI, monthly saving, total interest reduction, and break-even period. Use it before initiating any balance transfer conversation, with your existing lender or a new one.

MOD Charges Explained

MOD charges are the fees associated with creating and registering the mortgage document. They're not a single uniform fee; they're a combination of components, each with different recipients and different governing rules:

- Stamp duty

- Registration charges

- Documentation expenses

- Administrative fees

The exact amount varies from state to state because stamp duty laws are governed by individual state governments.

Typical MOD Charges in India

Most lenders calculate MOD charges as a percentage of the loan amount.

|

Loan Amount |

Approximate MOD Charges |

|

₹20 lakh |

₹10,000 to ₹40,000 |

|

₹40 lakh |

₹20,000 to ₹80,000 |

|

₹60 lakh |

₹30,000 to ₹1.2 lakh |

|

₹1 crore |

₹50,000 to ₹2 lakh |

Actual charges vary depending on state regulations, lender policies, and applicable stamp duty rates.

MOD Charges vs Other Home Loan Charges

Many borrowers confuse MOD charges with processing fees or registration expenses. However, they serve different purposes.

|

Charge Type |

Purpose |

Paid To |

|

MOD Charges |

Mortgage creation and registration |

Government and lender |

|

Processing Fee |

Loan application processing |

Bank or lender |

|

Property Registration Fee |

Property ownership registration |

Government |

|

Legal Verification Fee |

Property document verification |

Legal experts |

|

Technical Evaluation Fee |

Property valuation |

Valuation agency |

Understanding these differences helps borrowers prepare for the total cost of acquiring a property. MOD charges are specifically about the mortgage, the lender's security interest in the property. They're separate from the property's own registration (which registers ownership) and separate from the lender's processing fee (which covers loan evaluation). All four categories of charges MOD, processing, property registration, and legal and technical fees, typically apply to a home loan transaction and need to be budgeted for independently.

Also Read: Missed Your Home Loan EMI: How to Avoid ECS Penalties and Save Your CIBIL

Factors Affecting MOD Charges

Several factors influence the final MOD amount payable by borrowers.

1. State Government Rules

Stamp duty and registration rates differ across states. Some states charge a fixed percentage, while others have slab-based structures.

2. Loan Amount

Higher loan amounts generally attract higher MOD charges because fees are often calculated as a percentage of the sanctioned amount.

3. Type of Lender

Banks and housing finance companies may have different administrative and documentation charges.

4. Property Location

Certain states or local authorities may impose additional registration-related fees.

Benefits of MOD Registration

Although borrowers often see MOD charges as an additional expense, the registration provides important legal safeguards.

Legal Security

The mortgage becomes legally documented and enforceable.

Reduced Ownership Disputes

The registered mortgage establishes a clear record of lender rights.

Transparency

Both lender and borrower have documented evidence of the loan arrangement.

Easier Record Management

Property records remain properly documented throughout the loan tenure.

These protections benefit both parties and contribute to a smoother loan process.

Can MOD Charges Be Avoided?

No, if your lender requires MOD registration (and most do, particularly for larger loan amounts), the associated stamp duty and registration charges are mandatory government levies that cannot be waived. There's no negotiation with the state government on stamp duty.

- Asking for a detailed loan cost sheet before approval

- Understanding state-specific stamp duty rates

- Comparing charges among lenders

- Including MOD costs in their overall home-buying budget

Being aware of these charges beforehand helps prevent last-minute financial stress. Factor MOD charges into your budget from the beginning of your home purchase planning rather than discovering them at disbursement.

On a ₹60 lakh loan, MOD charges could add ₹30,000 to ₹1.2 lakh to your upfront costs depending on your state. That's a meaningful amount that should be in your cash flow plan, not a surprise.

Common Mistakes Homebuyers Should Avoid

Many borrowers overlook important details related to MOD charges.

Ignoring Additional Loan Costs

Focusing only on interest rates can lead to budget shortfalls during loan disbursement.

Not Verifying State Rules

MOD charges vary significantly across states.

Assuming Charges Are Refundable

In most cases, registration and stamp duty charges are non-refundable.

Forgetting to Budget for Documentation

Homebuyers should account for MOD charges alongside registration, legal, and processing fees.

Not Asking for Charge Breakup

Always request a detailed fee structure from the lender before signing loan documents.

Conclusion

A Memorandum of Deposit (MOD) charge is often kind of underestimated part of home loans in India it is a crucial component in the mortgage process because it forms a legal trail, for your loan known as mortgage, when your title documents are handed over to the lender, so in a way it offers a secure and legally safeguarded way for both the lender and borrower to deal with each other through the entire loan period.

MOD charges, while increasing the initial cost of borrowing, serve to create a legally binding mortgage agreement and safeguard both lender and borrower. Understanding these charges before signing a mortgage agreement will enable buyers to organize their finances better, giving them the chance to prevent any extra expenses arising during the property acquisition process. Consequently, every home loan applicant in 2026 must include MOD fees in their total home buying budget just as they would assess interest rates and monthly payments.

(1)_1784875521.webp)

Ans 1. MOD stands for Memorandum of Deposit, a legal document created when a borrower deposits their property's original title deeds with a bank or housing finance company as security for a home loan. The MOD formally records the mortgage arrangement between the borrower and lender, confirming that the property has been pledged as security until the loan is fully repaid. In many states, the MOD is registered with the Sub-Registrar's Office to create a public legal record. MOD charges are the stamp duty, registration fees, and administrative costs associated with creating and registering this mortgage document.

Ans 2. MOD charges in India in 2026 typically range from 0.1 to 0.5 percent of the loan amount, though actual amounts vary significantly by state due to different stamp duty regulations. For a ₹20 lakh loan, MOD charges range from approximately ₹10,000 to ₹40,000. For ₹40 lakh, the range is ₹20,000 to ₹80,000. For ₹60 lakh, charges range from ₹30,000 to ₹1.2 lakh. For ₹1 crore loans, MOD charges can range from ₹50,000 to ₹2 lakh. Your specific charge depends on the state where the property is located, the loan amount, and the lender's administrative fees.

Ans 3. Banks charge MOD fees because creating a legally valid, registered mortgage on the property requires payment of government stamp duty and registration charges; these are state government levies, not bank profits. The MOD registration establishes the lender's legal interest in the property as security for the loan and creates an official public record of the mortgage. Without the registered MOD, the lender's security interest in the property would be less legally robust and harder to enforce in case of default. The administrative component of MOD charges covers the bank's cost of preparing, handling, and filing the mortgage documentation.

Ans 4. MOD charges and property registration charges are distinct costs that serve different legal purposes. Property registration charges are paid to register the ownership transfer of the property, they record that the buyer has become the legal owner. MOD charges are paid to register the mortgage on the property; they record that the lender has a legal claim on the property as security for the home loan. Both involve the Sub-Registrar's Office and both involve stamp duty, but they relate to two separate legal transactions: the ownership transfer and the mortgage creation. Both sets of charges typically apply when a property is purchased with a home loan.

Ans 5. No, MOD charges are not refundable regardless of when the home loan is repaid. The charges cover stamp duty paid to the state government and registration charges paid for the official recording of the mortgage; these are government levies for the services rendered at the time of mortgage registration, not fees that can be refunded later. Whether you repay the loan in 5 years or 25 years, the MOD charges paid at loan disbursement are a one-time, non-refundable expense. What happens when the loan is repaid is that the lender executes a discharge of the mortgage, returns your original title deeds, and the mortgage entry in government records is updated to show the mortgage has been released.

Ans 6. Most banks and housing finance companies that require mortgage registration as part of their home loan process charge MOD fees. MOD charges include state government stamp duty and registration charges that are mandatory when the mortgage document is officially registered, these cannot be waived by any lender. Some lenders may waive the administrative component of their MOD charges as a promotional offer, but the government stamp duty and registration charges remain payable. If a lender claims to offer a "zero MOD charge" home loan, clarify specifically whether they mean the complete charge including stamp duty or only the lender's administrative fee component.

Ans 7. MOD charges are primarily calculated based on the state-specific stamp duty rate applied to the home loan amount. Most states levy stamp duty on mortgage documents as a percentage of the loan amount or the property value, whichever is applicable under the state's rules. Some states have slab-based structures with different rates for different loan amount ranges. Additional registration charges are applied on top of the stamp duty. The lender's administrative fee for document preparation and handling is also included in the total MOD charge. Because each state sets its own stamp duty rate independently, the MOD charge on the same loan amount can vary considerably from state to state.

Ans 8. When a home loan is fully repaid, the lender executes a formal discharge of the mortgage, a Memorandum of Discharge or No Objection Certificate confirming the loan has been repaid in full. The lender returns all original title deed documents that were deposited at the time of the loan. The mortgage registration entry is updated through the appropriate authority to reflect that the mortgage has been discharged. Once this process is complete, the property is free of the lender's claim and the borrower holds full, unencumbered ownership. Borrowers should ensure they receive all original documents and the formal discharge documentation for their records.

Ans 9. MOD charges and other upfront loan costs are typically not included in the principal home loan amount, they are out-of-pocket expenses payable by the borrower at the time of loan disbursement. The home loan amount is generally limited to a percentage of the property's value (typically 75 to 90 percent depending on the loan amount), which is intended to cover the property purchase price. Additional costs including MOD charges, stamp duty, processing fees, and legal fees must be paid from the borrower's own funds. Borrowers should budget for these upfront costs separately from the down payment when planning their home purchase finances.

Ans 10. The documents involved in MOD registration for a home loan include the original title deeds and ownership documents of the property being mortgaged, the home loan sanction letter specifying the approved loan amount and terms, identity proof of the borrower, the Memorandum of Deposit document prepared by the lender's legal team, and any additional documents required by the specific state's stamp duty and registration authority. The exact documentation requirements vary by state and lender. The bank's legal team or home loan coordinator typically guides the borrower through the specific documents needed for the MOD registration in their state.