When it comes to borrowing money or taking out a loan, understanding the different interest rate structures is essential. Two common types are the flat rate and the reducing rate. Each structure offers distinct advantages and drawbacks. This article will delve into both flat rate and reducing rate interest structures, highlighting their benefits and disadvantages, key considerations, and frequently asked questions.

Flat Rate Interest

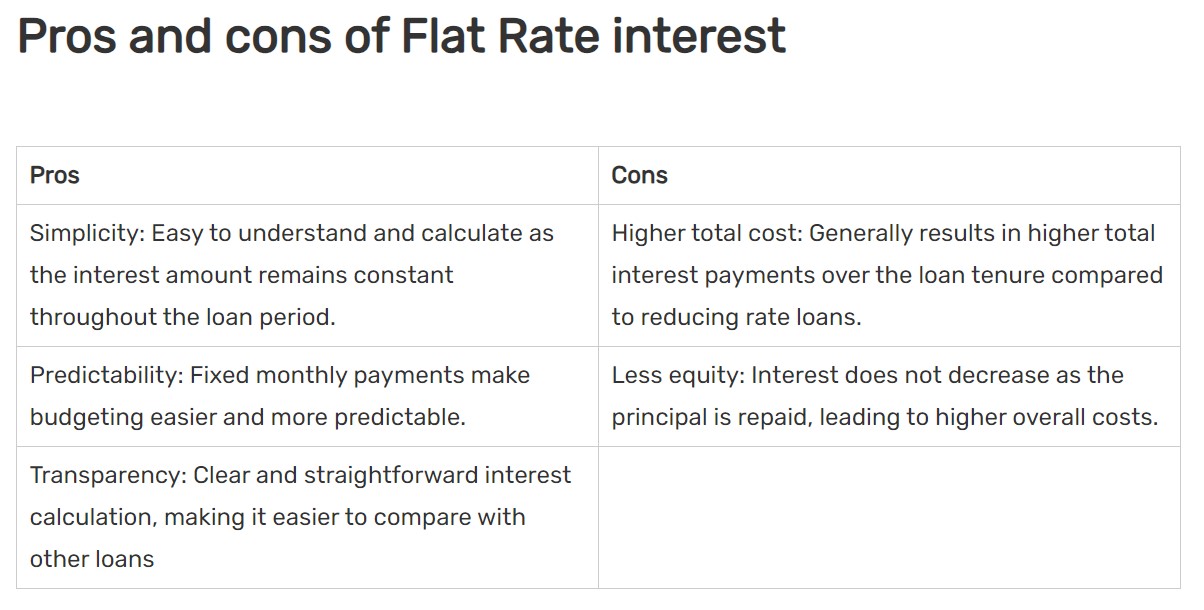

Flat rate interest is a straightforward method of calculating interest where the amount is based on the original principal throughout the entire loan period. This means the interest remains constant regardless of how much of the principal has been repaid.

How It Works

For instance, if you take out a loan of ₹10,000 at a flat rate of 10% per annum for 5 years, the interest is calculated as follows:

Annual Interest=Principal×Ratetext{Annual Interest} = text{Principal} times text{Rate}Annual Interest=Principal×Rate Annual Interest=10,000×0.10=₹1,000text{Annual Interest} = 10,000 times 0.10 = ₹1,000Annual Interest=10,000×0.10=₹1,000

So, over the 5-year term, the total interest would be:

1,000×5=₹5,0001,000 times 5 = ₹5,0001,000×5=₹5,000

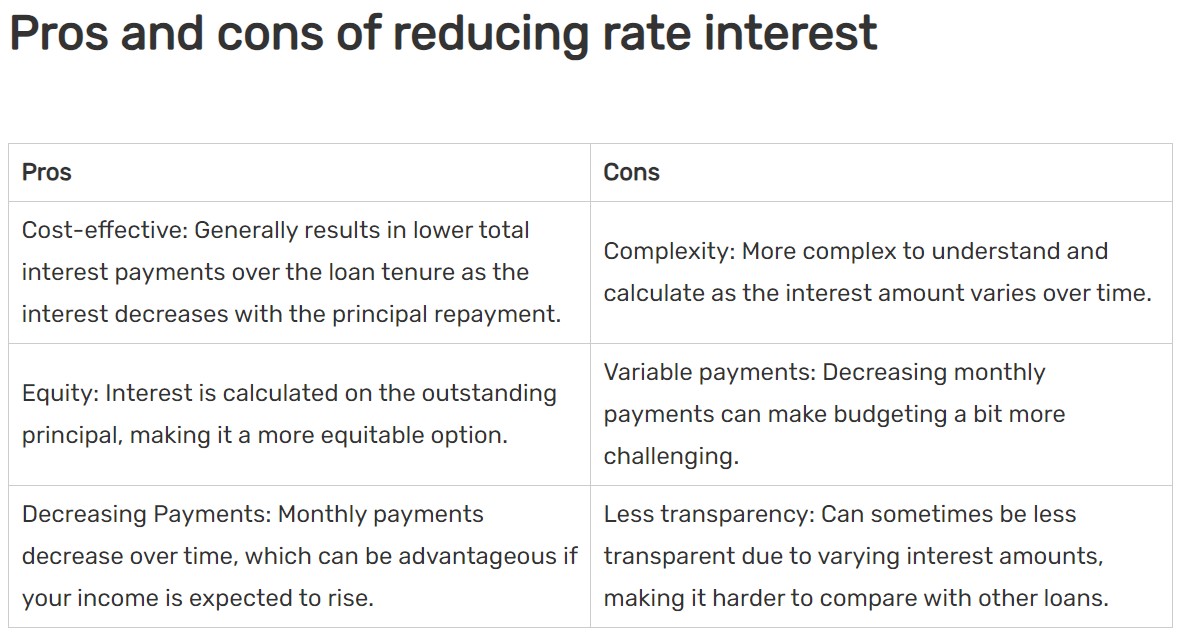

In contrast, a reducing rate interest—also known as a declining balance interest—is calculated based on the outstanding principal amount. As you make repayments, the principal decreases, leading to a reduction in the interest amount. This method is often regarded as more fair and can result in a lower total interest paid over the course of the loan.

How It Works

Using the same example of a ₹10,000 loan at a reducing rate of 10% per annum for 5 years, the interest calculation differs significantly. In the first year, the interest would be:

Interest for Year 1=Principal×Ratetext{Interest for Year 1} = text{Principal} times text{Rate}Interest for Year 1=Principal×Rate Interest for Year 1=10,000×0.10=₹1,000text{Interest for Year 1} = 10,000 times 0.10 = ₹1,000Interest for Year 1=10,000×0.10=₹1,000

If you repay ₹2,000 at the end of the first year, the outstanding principal for the second year would be:

When choosing between flat rate and reducing rate interest structures, it's crucial to consider the following factors:

Loan Tenure The length of the loan significantly affects the total interest paid. Flat rate loans can become more costly over longer periods, while reducing rate loans tend to save you money as the interest decreases over time.

Monthly Repayments Flat rate loans offer consistent monthly payments, making budgeting easier. In contrast, reducing rate loans have decreasing payments, which might be beneficial if you expect your income to grow.

Total Cost The overall expense of the loan is a key factor. Reducing rate loans generally result in lower total interest payments compared to flat rate loans, making them more cost-effective in the long term.

Transparency Understanding the true cost of a loan can be challenging. Reducing rate loans can sometimes be less transparent due to fluctuating interest amounts, whereas flat rate loans provide simplicity with fixed interest payments.

Prepayment Penalties Some loans have penalties for early repayment. It's important to review the loan terms to understand any potential costs associated with paying off the loan ahead of schedule.

Purpose of the Loan The intended use of the loan can also influence your choice. For short-term loans or smaller amounts, a flat rate might be simpler and more straightforward. For larger, long-term loans, a reducing rate can offer significant savings.

Choosing between flat rate and reducing rate interest structures involves evaluating factors such as loan tenure, monthly repayment capabilities, total cost, and transparency. While flat rate loans offer predictability, reducing rate loans can be more economical over time. By understanding these differences and considering your specific needs, you can make an informed decision that aligns with your financial goals.

Ans 1. Flat Interest Rate

The financial organization decides on the repayment schedule and decides the EMIs payable by the borrower. It also keeps the total repayment liability fixed for a borrower and helps plan finance beforehand. Flat interest rates effectively remain higher than reducing rates.

Ans 2. Floating rates are slightly lower than fixed rates. If you are comfortable with the prevailing interest rates, are reasonably sure that interest rates will rise in future, opt for a fixed rate home loan. If you are unsure about where interest rates are heading, opt for a floating rate home loan.

Ans 3. Lower interest rates, for example, often encourage more people to obtain a mortgage for a home or to borrow money for an automobile or home improvements. Lower rates also can encourage businesses to borrow funds to invest in expansion, such as purchasing new equipment, updating plants, or hiring more workers.

Ans 4. It depends on whether you're saving or borrowing. Compound interest is better for you if you're saving money in a bank account or being repaid for a loan. If you're borrowing money, you'll pay less over time with simple interest.

Ans 5. When a loan is fixed for its entire term, it remains at the then-prevailing market interest rate, plus or minus a spread that is unique to the borrower. Generally speaking, if interest rates are relatively low, but are about to increase, then it will be better to lock in your loan at that fixed rate.

Author: Neha Kapoor

Neha Kapoor is a taxation and finance consultant with 8+ years of experience in income tax planning, filing, and compliance advisory. She simplifies complex tax laws, deductions, and government policies, helping individuals and businesses stay compliant while saving money. Her insights empower readers to make informed financial and tax-related decisions with confidence.

Ans 1. Flat Interest Rate The financial organization decides on the repayment schedule and decides the EMIs payable by the borrower. It also keeps the total repayment liability fixed for a borrower and helps plan finance beforehand. Flat interest rates effectively remain higher than reducing rates.

Ans 2. Floating rates are slightly lower than fixed rates. If you are comfortable with the prevailing interest rates, are reasonably sure that interest rates will rise in future, opt for a fixed rate home loan. If you are unsure about where interest rates are heading, opt for a floating rate home loan.

Ans 3. Lower interest rates, for example, often encourage more people to obtain a mortgage for a home or to borrow money for an automobile or home improvements. Lower rates also can encourage businesses to borrow funds to invest in expansion, such as purchasing new equipment, updating plants, or hiring more workers.

Ans 4. It depends on whether you're saving or borrowing. Compound interest is better for you if you're saving money in a bank account or being repaid for a loan. If you're borrowing money, you'll pay less over time with simple interest.

Ans 5. When a loan is fixed for its entire term, it remains at the then-prevailing market interest rate, plus or minus a spread that is unique to the borrower. Generally speaking, if interest rates are relatively low, but are about to increase, then it will be better to lock in your loan at that fixed rate.