Choosing Between a Bank and a Housing Finance Company for Your Home Loan

Deciding where to secure your home loan can be challenging. Should you opt for a loan from a bank or a housing finance company (HFC)? Both options have their advantages and disadvantages. Let’s explore which might be the best fit for you.

When it comes to financing your home purchase, you have options. You can either turn to banks or housing finance companies for your home loan. Owning a home is a significant milestone, providing stability, joy, and security. Understanding your financing options can help you make an informed decision.

What Are Housing Finance Companies (HFCs)?

Housing Finance Companies (HFCs) are regulated by the Companies Act of 1956 and the Reserve Bank of India (RBI) since 2019. They were established to specifically offer home loans, easing the load on traditional banks and providing consumers with additional choices.

Advantages and Disadvantages of Home Loans from Banks vs. HFCs

Here’s a closer look at the pros and cons of obtaining a home loan from a bank compared to an HFC:

Advantages of Home Loans from Housing Finance Companies:

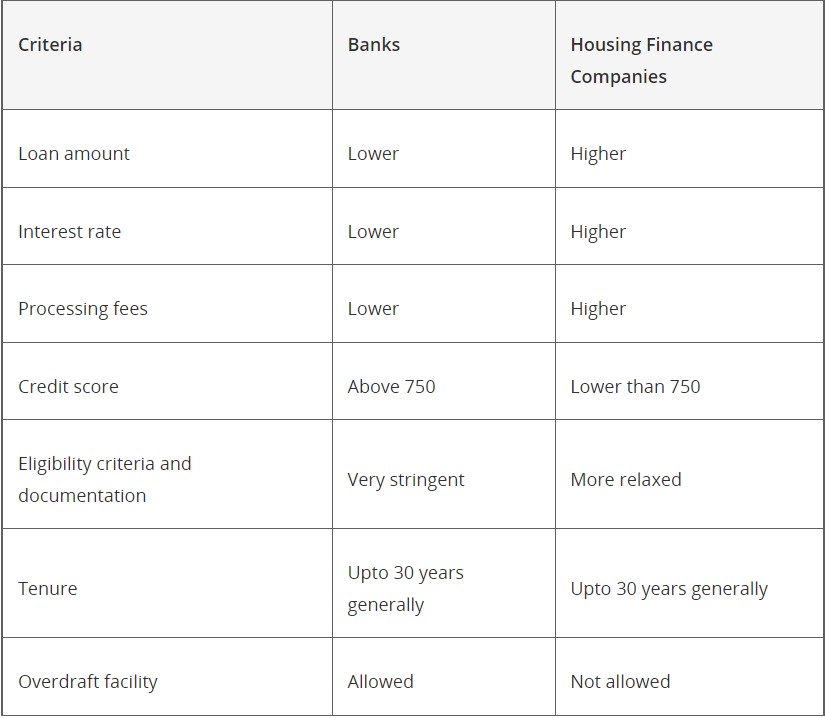

Higher Loan Amounts HFCs often consider additional costs like stamp duty and registration fees when evaluating your property, which means they may approve larger loan amounts compared to banks that typically exclude these expenses.

Flexible Credit Score Requirements HFCs are generally more flexible regarding credit scores. While they may charge higher interest rates, they are willing to lend to individuals with lower credit scores, unlike banks that might be stricter.

Simplified Loan Application Process The loan application process with HFCs is usually more streamlined and faster due to simpler documentation requirements. Banks often have a more rigorous paperwork process, which can delay loan approvals.

Relaxed Eligibility Criteria HFCs tend to have more lenient eligibility criteria. They are more likely to approve loans for self-employed individuals, early-stage entrepreneurs, artists, and freelancers who may not have a steady income, whereas banks might be more restrictive.

Understanding these factors can help you choose the right lender based on your specific needs and financial situation. Both banks and HFCs have unique advantages, so consider what matters most to you in securing your home loan.

Disadvantages of Home Loans from Housing Finance Companies

While Housing Finance Companies (HFCs) offer several benefits, they also have some drawbacks compared to traditional banks. Here’s a look at some of the disadvantages:

Higher Interest Rates HFCs often borrow funds from banks, which means they tend to charge higher interest rates on home loans. As a result, you may end up paying more in interest over the life of the loan compared to a bank loan.

Fewer Branches There are fewer HFCs and branches compared to banks, which can make it more challenging to find a nearby office or get in-person assistance.

Higher Processing Fees HFCs generally charge higher processing fees for home loans compared to banks. This can increase the overall cost of obtaining a loan through an HFC.

Understanding these potential downsides can help you make a more informed decision when choosing between a bank and a housing finance company for your home loan.

Pros and Cons of a Home Loan from a Bank vs Housing Finance Company

Here are the main reasons people want to go for a home loan from a bank vs housing finance company.

When choosing between a bank and a Housing Finance Company (HFC) for a home loan, here are some advantages of opting for a bank:

Lower Interest Rates Banks generally offer lower interest rates on home loans compared to HFCs. This is because banks have stricter lending criteria, which allows them to afford lower rates.

MCLR Regulation Banks are required by the RBI to follow the Marginal Cost of Funds based Lending Rate (MCLR) for setting interest rates. Any changes in the RBI’s repo rate directly impact the MCLR and, consequently, the interest rate on your home loan. This means if the repo rate drops, your loan interest rate may decrease, benefiting you as a borrower. In contrast, HFCs usually link home loans to their own benchmark prime lending rate, which doesn’t fluctuate as frequently. Therefore, changes in interest rates are less common with HFCs.

Developer Partnerships Banks often have tie-ups with property developers, offering special deals and discounts on loans when you purchase property from these developers. These partnerships can enhance your overall property-buying experience and financial planning.

Widespread Availability Nationalized banks are widespread across India, making it easy to visit a branch for loan inquiries or documentation. The convenience of having numerous branches nearby ensures that you can handle paperwork and other requirements without significant travel.On the other hand, HFCs have fewer branches, which can make accessing services more difficult if a branch is not conveniently located.

Overdraft Facility Banks often provide overdraft facilities, which can be especially useful if you need additional funds for emergencies or significant expenses, such as medical bills or educational fees. With an overdraft facility, you can withdraw a sum of money and only pay interest on the amount you use, rather than taking out a separate loan and paying interest on both. This can result in lower overall interest payments compared to managing multiple loans.

Understanding these advantages can help you make an informed decision when selecting a home loan provider.

Disadvantages of Banks

Banks want high credit score on CIBIL

They do a very rigorous due diligence

The eligibility criteria set by banks have many factors

The documentation process is extensive

Home Loan from a Bank vs Housing Finance Company - Comparative Analysis

Home Loans from Different Types of Banks: An Overview

In India, there are three main types of banks to consider for home loans: Public Sector Banks (PSUs), Private Banks, and Co-operative Banks. Each type has its own features, which can influence your decision when comparing home loan options with housing finance companies (HFCs).

Public Sector Bank Home Loans: Features

Lower Interest Rates: PSUs, backed by the government, typically offer lower interest rates compared to private and co-operative banks.

Special Benefits: They often have special schemes for women, senior citizens, government employees, and other groups.

Processing Time and Fees: Processing times and fees are generally moderate.

Higher Interest Rates: Private banks usually have higher interest rates compared to PSUs and co-operative banks.

Faster Processing: They often provide quicker loan approval and disbursal.

Personalization Options: Private banks offer various customization options such as top-up loans, balance transfers, and multiple repayment modes.

Promotional Rates: To attract customers, private banks frequently offer seasonal or promotional interest rates.

Co-operative Bank Home Loans: Features

Lower Processing Fees: Co-operative banks typically have lower processing fees and charges than larger banks.

Local Accessibility: They are more accessible to local residents and can be a good option for those needing smaller loan amounts.

Flexible Terms: Loan terms can be more flexible, as these banks aim to support the local community financially.

Interest Rates: Interest rates are based on the Prime Lending Rate and are generally higher than those offered by PSU banks.

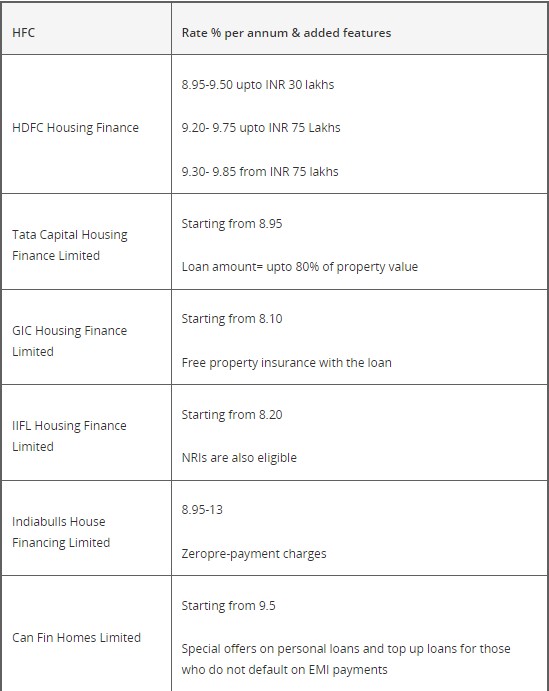

Top Housing Finance Companies in India

If you’re considering a home loan from a housing finance company instead of a bank, it’s essential to compare the interest rates and features offered by leading HFCs. This will help you make an informed choice based on your specific needs and preferences.

Conclusion to Home Loan from a Bank vs Housing Finance Company

Both banks and housing finance companies (HFCs) offer excellent options for home loans, each with its own set of benefits and trustworthy services. The best choice depends on your specific needs and expectations for the loan.

It’s important to discuss your options with your family and seek advice from those with experience in home financing to make an informed decision.

We hope this blog has provided you with valuable insights into the factors to consider when choosing between a home loan from a bank and one from an HFC.

Ans 1. Difference Between HFC vs.HFCs display high flexibility in loan approval, with a streamlined and uncomplicated process. Banks provide overdraft facilities based on regular EMI payments and a favorable CIBIL record. HFCs do not offer overdraft or credit facilities for their sanctioned loans.

Ans 2. Ultimately, the choice of in-house versus bank financing falls on the financial capability of the buyer. While banks offer the best interest rates, in-house financing offers an alternative for those who are not qualified or have had their bank loans disapproved.

Ans 3. Significant differences between banks and NBFC home loanWhile banks often offer lower interest rates due to their access to low-cost funds, NBFCs can be more flexible in terms of eligibility and documentation requirements.

Ans 4. Is HFC connection Good? While HFC connection is not as good or reliable as fibre to the premises connections (FTTP), it is affordable and better than FTTN and FTTC.

Ans 5. The best option for you depends on your specific circumstances. If you lack credit history or have poor credit it may be easier to get a loan from a private lender. If you have a good credit score or an established relationship with a bank, you will likely qualify for better lending terms.

Author: Neha Kapoor

Neha Kapoor is a taxation and finance consultant with 8+ years of experience in income tax planning, filing, and compliance advisory. She simplifies complex tax laws, deductions, and government policies, helping individuals and businesses stay compliant while saving money. Her insights empower readers to make informed financial and tax-related decisions with confidence.

(1)_1784875521.webp)

Ans 1. Difference Between HFC vs.HFCs display high flexibility in loan approval, with a streamlined and uncomplicated process. Banks provide overdraft facilities based on regular EMI payments and a favorable CIBIL record. HFCs do not offer overdraft or credit facilities for their sanctioned loans.

Ans 2. Ultimately, the choice of in-house versus bank financing falls on the financial capability of the buyer. While banks offer the best interest rates, in-house financing offers an alternative for those who are not qualified or have had their bank loans disapproved.

Ans 3. Significant differences between banks and NBFC home loanWhile banks often offer lower interest rates due to their access to low-cost funds, NBFCs can be more flexible in terms of eligibility and documentation requirements.

Ans 4. Is HFC connection Good? While HFC connection is not as good or reliable as fibre to the premises connections (FTTP), it is affordable and better than FTTN and FTTC.

Ans 5. The best option for you depends on your specific circumstances. If you lack credit history or have poor credit it may be easier to get a loan from a private lender. If you have a good credit score or an established relationship with a bank, you will likely qualify for better lending terms.