Table of Content

▲

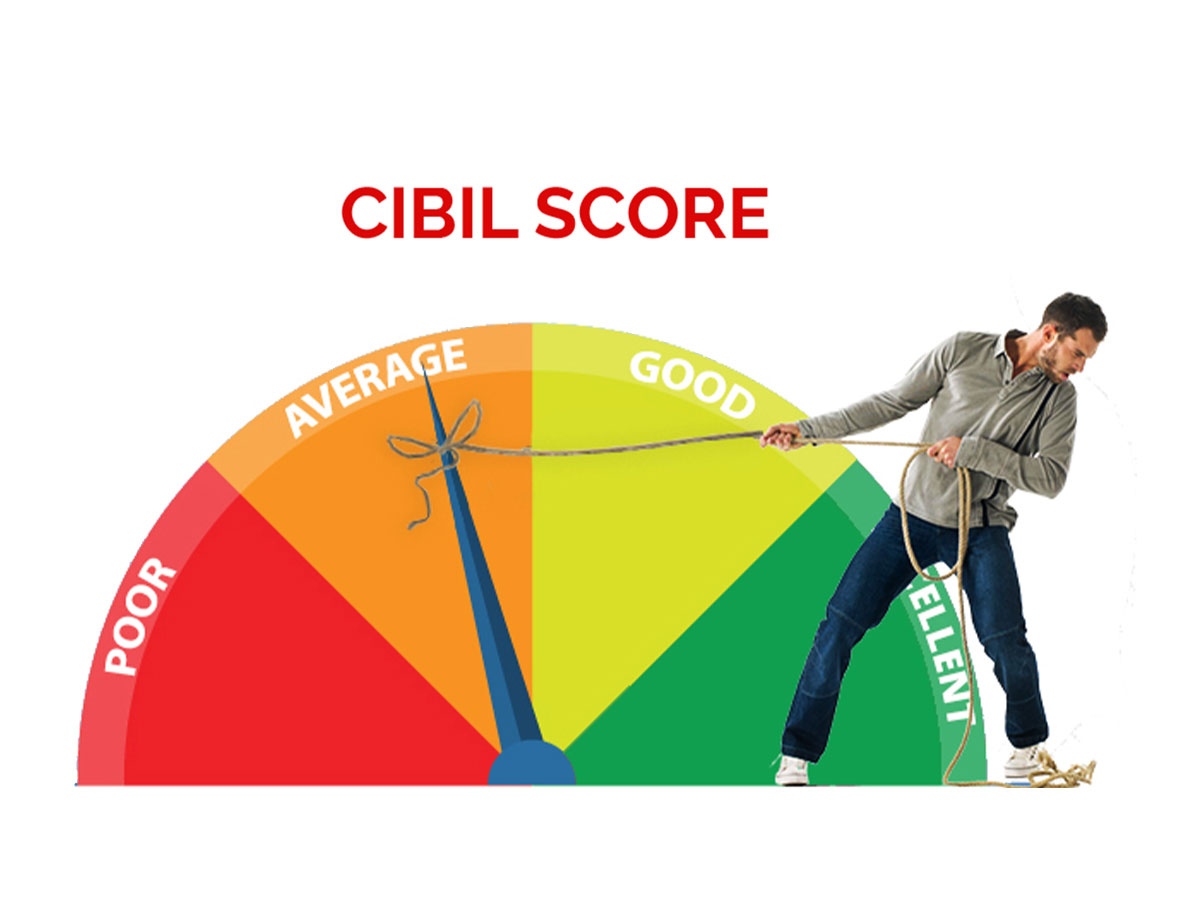

Are you aware that the CIBIL Score or credit score plays a pivotal role in the approval of a home loan? A favorable credit score is essential for securing a home loan, and if your credit score falls within the poor range, the chances of loan rejection by the bank increase. Typically, a good credit score falls between 750-900, reflecting a strong creditworthiness. On the contrary, a credit score below 500 is categorized as poor, which can significantly impact the approval process for a home loan. It's crucial to maintain a positive credit history and ensure a credit score within the acceptable range to enhance the likelihood of securing a home loan successfully.

|

Credit Score |

Rating |

|

300-500 |

Poor |

|

500-650 |

Average |

|

650-750 |

Good |

|

750-900 |

Excellent |

What is CIBIL score?

The CIBIL Score is a credit assessment provided by TransUnion CIBIL to individuals and businesses, serving as a measure of their creditworthiness, especially in the context of securing a Home Loan. Financial institutions and banks use the CIBIL Score to evaluate the feasibility of granting a Home Loan to a specific individual. This numerical score, ranging between 300 and 900, is calculated based on the individual's credit history, encompassing the borrowing and repayment patterns.

A higher CIBIL score enhances the likelihood of an individual being approved for a Home Loan, indicating a more favorable credit profile. Beyond the CIBIL score, lenders also take various other factors into consideration when determining an applicant's eligibility for a Home Loan. These factors collectively contribute to the comprehensive assessment conducted by financial institutions to gauge the creditworthiness and repayment capability of individuals seeking a Home Loan. For a deeper insight into the significance of different credit scores and their impact on securing a Home Loan, additional information can be found in the provided link.

How is CIBIL Score Calculated?

In the computation of the CIBIL Score, a thorough analysis of the individual's complete credit history is undertaken. This analysis encompasses various elements such as the total number of loans availed, including those associated with credit cards, and the consistency in repaying these loans. Additionally, other relevant parameters related to credit activities are taken into account. The evaluation of these parameters is conducted based on the assigned weightage to each, considering the applicant's performance in meeting the criteria for each parameter. This comprehensive assessment provides a nuanced understanding of the individual's credit behavior and financial responsibility, contributing to the final CIBIL Score that reflects their creditworthiness.

4 Major Factors for Calculating the CIBIL Score:

- Past Performance: Past Performance has 30% weightage to the overall score.

The past repayment record of the loans and credit cards availed by the applicant is considered, and this is considered as the most important criterion in calculating the score.

Visible patterns of irregularity in payment of EMIs or credit card dues decrease the score on this parameter. Missed or bounced EMIs, and credit card dues paid after due date results in a lower score.

It is to be noted that missing just one EMI or delaying credit card dues by 30 days does not lower the score. Payments delayed once or twice in 2-3 years do not significantly affect the CIBIL score.

But, repeated instances of irregular payment including missing EMIs for 2-3 months consecutively or delaying payment of credit card dues by 60-90 days causes the CIBIL score to go down by around 100 points.

Additionally, missing more than 3 EMIs, or delaying credit card dues by more than 90 days, results in involving recovery agents by the banks, which significantly reduces the CIBIL score which CANNOT BE CORRECTED FOR 7 YEARS!

However, EMI holidays and moratorium availed, such as the one offered during the COVID-19 pandemic, does not account for irregular payments.

- Credit Type and Duration: This has 25% weightage to the overall score

This parameter has two parts- one which represents whether the credit availed was secured or unsecured; and the total duration since the first credit availed by the person.

A secured credit refers to a loan taken against any asset. In simple terms, the lenders can sell-off the asset in case of loan default. E.g. Car Loan, Two

Wheeler Loan, Home Loan, etc. Unsecured loan refers to a loan taken without any end-use restriction. E.g. Personal Loan, Credit Card, etc.

Wheeler Loan, Home Loan, etc. Unsecured loan refers to a loan taken without any end-use restriction. E.g. Personal Loan, Credit Card, etc.

It is advisable to have a balance of secured as well as unsecured credit. However, more of unsecured credit also contributes to a lower score.

Further, the availability of a steady credit history for at least 24 months adds to the overall score. It signifies that the applicant is used to taking credit and is familiar with its repayment.

- Credit Exposure: Credit Exposure accounts for25% weightage to the overall score

It is also called Credit utilization Ratio. It is the ratio of the total spends to the total available credit limit. In simple terms, the credit exposure represents the dependency of the person on credit for living his/her life.

While a credit exposure of 30% is considered ideal, a higher credit exposure ratio is considered negative and causes the score to lower down significantly.

- Other Parameters: These parameters account for the remaining 20% weightage

These include parameters such as the number of loans or credit cards applied, and recent repayment trends (around the latest six months), among others. A high number of loans or credit cards applied within a short time (around 6-12 months), irrespective of those being sanctioned, lower the credit score.

In simple terms, even applying repeatedly for loans adversely affects the credit score. The Ideal CIBIL Score

The CIBIL score, ranging from 300 to 900, signifies the creditworthiness of an individual, with 300 being the lowest and 900 the highest. A higher score correlates with an increased likelihood of a successful home loan approval.

Banks typically desire a minimum CIBIL score within the range of 700-750 for the sanction of a Home Loan. While specific criteria may vary among banks, a score of at least 700 is a common requirement in India.

Individuals with a credit score falling between 650-700 are deemed moderately risky by banks, which might result in eligibility for a reduced Home Loan amount or higher interest rates compared to applicants with scores above 700. Scores below 650 are considered high risk, and lenders may be hesitant to approve Home Loans for such applicants.

Despite this, credit scores below 650 can be improved to levels acceptable by banks. Various methods, including regularizing credit repayments, settling outstanding loans promptly, and observing a waiting period of 6-12 months before applying for a fresh loan, can contribute to score improvement.

Instances of delayed loan repayments due to genuine and unavoidable circumstances, such as technical errors or delays in receiving credit card statements, may adversely impact the CIBIL Score. In such cases, individuals can initiate a Credit Repair request with CIBIL, providing details of the delay instances, to request a revision of their CIBIL score.

Benefits of Having a Good CIBIL Score

A good CIBIL score is always beneficial and gives an edge to the loan buyer. Here are some benefits of having a good CIBIL score:

- The loan buyer holds better or more negotiating power if he/she has a good CIBIL score

- Having a good CIBIL score also helps you in taking a home loan at highly nominal interest rates

- You can negotiate and get the desired home loan amount sanctioned

- Having a good CIBIL score helps in fastening up the loan approval and disbursal process

Factors Impacting Your CIBIL Score

A vital factor that decides whether or not you can avail of a loan is your credit score, also called the CIBIL score. Based on your past financial behaviour and credit history, the CIBIL score calculates your creditworthiness. Therefore, it is crucial to maintain a good CIBIL score for better chances of getting a loan. Here are some factors that can impact your credit score-

- A poor loan repayment history, be it late repayment or a higher number of defaults, can impact your CIBIL score negatively.

- If you already have two or three loans, i.e., a large amount of debt, it will decrease your CIBIL score.

- Making multiple loan applications can also negatively affect your CIBIL score. Thus, it is recommended that you only enquire if you need a loan.

- Borrowing just one type of credit can affect your CIBIL; therefore, take different kinds of credit, including secure and unsecured loans.

- If you use credit to the maximum extent, it gives the impression that you are credit-hungry. Therefore, your CIBIL score drops.

One must consider the above-mentioned factors to ensure a good CIBIL Score.

Low CIBIL Score - Can I Still Get a Loan?

Securing a loan with a low CIBIL score is feasible, but it can be a cumbersome process. A low CIBIL score indicates a higher risk of payment default, leading to potential complications. In such instances, various scenarios may unfold, including the requirement to provide additional documents, facing higher interest rates imposed by lending banks, or encountering challenges in obtaining the desired loan amount.

To mitigate these challenges, it is crucial to adhere to sound financial practices and strive to maintain a favorable CIBIL score. By doing so, individuals can enhance their creditworthiness and streamline the loan application process, ensuring a smoother and more favorable experience with lending institutions.

CIBIL Score for people with no credit history

Moreover, for some individuals with no or limited credit history available, the credit score may range from -1 to 5, based on their risk factor as assessed by CIBIL. These include:

- First-time borrowers and applicants whose credit history is not available for more than six months. Such cases are referred to as No History (NH), and the applicants are granted a score of -1 (minus one).

- Applicants who have no loan or credit card repayment record for the last 24 months. Such applicants are granted a score of 0 (zero), and termed as Credit History Not Available (NA).

In such cases, the company uses the CIBIL TransUnion 2.0 method to calculate a score of 1-5 based on the risk factor of the individual. A score of 1-2 represents the least risk of a loan default, 3 represents a moderate risk, and 4-5 represents the highest risk of default.

Various factors including age, income, marital status, education, last six months’ repayment record, and recent loan applications, etc. are taken into consideration in CIBIL TransUnion 2.0

Some Tips for Having a Good CIBIL Score

- Make sure to have sufficient balance in the bank account to avoid any EMI bounce

- Pay your credit card dues in full. AVOID PAYING JUST THE MINIMUM AMOUNT EVERY MONTH. As far as possible, maintain a NIL/ minimum Credit Balance at all times.

- Pay your credit card dues before the due date. Don’t delay it till the last date.

- Don’t exhaust your credit limit. Spend only up to 40% of your credit limit.

- Avoid taking multiple loans and credit cards. It is always advisable to take a secured loan rather than an unsecured loan like personal loans and credit cards

- If you have been declined a loan or credit card, DO NOT REPEATEDLY APPLY FOR THE SAME WITH DIFFERENT BANKS FOR A YEAR.

Wrapping Up: How is CIBIL Score calculated for Home Loan

The term "CIBIL score" is synonymous with "credit score," and it holds significant importance in the approval process of a home loan. A favorable credit score not only facilitates loan approval but can also result in a lower interest rate. Conversely, individuals with poor credit scores may encounter higher interest rates. Various factors impact the CIBIL score, including defaults in credit card payments, delayed loan EMIs, or hard inquiries.

It is strongly recommended to assess your credit score before applying for a home loan. This proactive step allows individuals to gauge their creditworthiness and take measures to improve or maintain a favorable credit score, ultimately contributing to a more favorable lending experience.

Also Read: Home Loan from Public Sector Bank Vs Private Sector Bank

Ans 1. between 720 and 750Ideal credit score to avail a personal loanThe minimum CIBIL score for a personal loan is between 720 and 750. Having this score means you are creditworthy, and lenders will approve your personal loan application quickly. They may also offer you your chosen loan amount at a nominal interest.

Ans 2. If you have a CIBIL score that is within a range of 651-750, you may still get a loan, but chances are that it may attract a higher interest rate and you may have to repay it over a shorter repayment tenure. Meanwhile, If your score is lower than 650, it may prove difficult for you to get a personal loan.

Ans 3. You can get a personal loan with an 720 credit score, but not every lender may approve you. Some lenders require scores well into the 700s for consideration. However, depending on the lender, you may get a personal loan with rather competitive terms.

Ans 4. 300 to 900A CIBIL score goes from 300 to 900, with the highest score being 900. Individuals having a CIBIL score of 750 or higher are generally regarded as responsible borrowers.

Ans 5. One of the main reasons for CIBIL score drop may be non-payment/delayed payment of credit card bills. Paying off outstanding credit card bills on time can help individuals to increase their credit scores.